Trump Threatens 100% Tariffs on Countries Imposing Digital Services Taxes on U.S. Tech Firms

Trump Threatens 100% Tariffs on Countries Imposing Digital Services Taxes on U.S. Tech Firms  Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  South Korea’s KOSPI Jumps Over 5% as Samsung, SK Hynix Rally on Micron Earnings Boost

South Korea’s KOSPI Jumps Over 5% as Samsung, SK Hynix Rally on Micron Earnings Boost  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Gold Prices Fall Below $4,000 as Strong Dollar, Fed Rate Hike Bets Weigh on Bullion

Gold Prices Fall Below $4,000 as Strong Dollar, Fed Rate Hike Bets Weigh on Bullion  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Iran Attack in Strait of Hormuz Pushes Oil Prices Higher

Iran Attack in Strait of Hormuz Pushes Oil Prices Higher  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Gold Prices Rise Above $4,000 as Inflation Data and Weaker Dollar Boost Demand

Gold Prices Rise Above $4,000 as Inflation Data and Weaker Dollar Boost Demand  S&P Affirms Brazil’s BB Credit Rating with Stable Outlook Amid Fiscal Challenges

S&P Affirms Brazil’s BB Credit Rating with Stable Outlook Amid Fiscal Challenges  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  Asian Stocks Sink as Apple Price Hikes Spark AI Valuation Fears, South Korea and Japan Lead Selloff

Asian Stocks Sink as Apple Price Hikes Spark AI Valuation Fears, South Korea and Japan Lead Selloff  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch

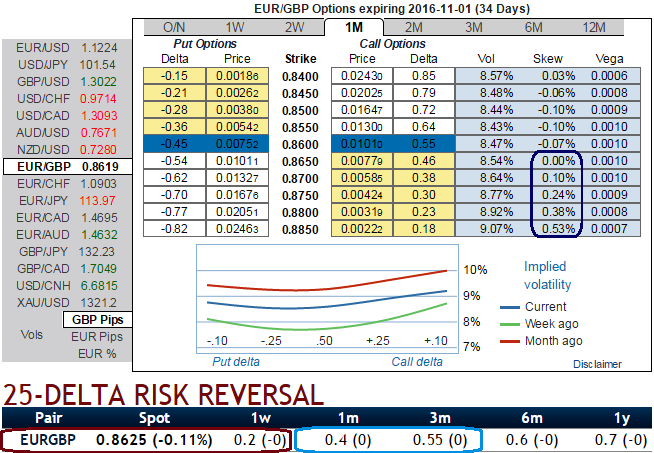

This week, although EURGBP is losing in its price, we remain bearish of GBP, and forecast a 5-10% move from here in GBP/USD, taking the pair below 1.25, taking EUR/GBP to a little above 0.90. EURGBP was at 0.8616 from yesterday’s close at 0.8613.

That justifies GBP shorts, but the appeal of EURGBP long is not so much our expectation of a circa 5% move higher over time, but the potential for a much bigger move if the Euro rallies across the board after a long period of sideways trading.

Parity is reachable The Euro’s sharp fall in 2014-2015 was caused by the divergence between Fed and ECB policy, which widened interest rate differentials, but also by the ECB’s bond-buying operations, which had a huge impact on capital flows from Europe.

German business confidence improved much more than expected in September, as uncertainty over Britain's vote to exit the European Union abated, industry data showed on Monday.

OTC Outlook and Hedging Strategy:

OTC outlook and hedging strategy:

Delta risk reversals of EURGBP: From the nutshell showing delta risk reversals of EURGBP, you can probably make out that the pair has been one of the most expensive pairs to be hedged for upside risks as it indicates calls have been relatively costlier over puts but negative hedging sentiments in 1 week’s tenor

Needless to specify, GBP vols have still been flying high pace no matter what both prior and post-Brexit events, but this time, these IVs are also owing to BOE’s monetary policy decision.

So it is advisable to initiate Diagonal Credit Call Spread (DCCS) in order to tackle both short-term dips and major uptrend.

Execution: Keeping the above fundamental factors in mind, it is advisable to go long in 1M (1%) OTM 0.36 delta call while writing 1W (1%) ITM call with positive theta and delta closer to zero (both sides use European style options), this credit call spread option trading strategy is recommended when the underlying spot FX price is anticipated to drop moderately in the near term and spikes up in long term.

Usually, pondering over the option sensitivity tool, IVs and OTC indications these puzzling could be optimally tackled and attained the trade or investment objectives via theta options of shorter tenors.

Option sellers can reap the benefits of a high Theta near expiry by selling short-dated ATM options with the expectation of little to almost no market movement.

For ITM and OTM options as the time to expiry draws nearer, Theta lowers and decreases. One can understand from the IV and risk reversal nutshell that 1w tenor signifies bears hedging interests and so is the sentiments in the long run.