Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

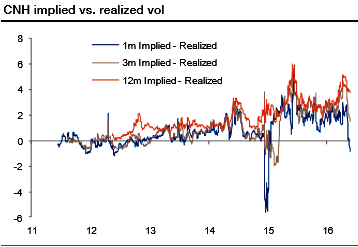

The premium of implied volatility to realized has fallen across tenors; most notably at the front-end where the 1m spread has declined by 2.5 vol points (now in negative territory) and in 3m which is 3 vol points lower from the recent high.

Further out the curve, the gap between 1y implied and realized vol is down 1.1 vol points but still remains elevated on a historical basis. This suggests continuing to favor short volatility structures that benefit from RMB weakness.

Since the depreciation phase in 2014 it has been a rare occurrence for CNH to trade at a premium to CNY.

CNH premium over CNY is 50bp (i.e. USDCNH is 50bp lower than USDCNY), while CNH vol is only slightly higher than CNY (0.2-0.3 vol points).

In the 1-3m tenor it is cheaper to short RMB via CNY NDF’s (100-300bp) but from 6m-12m the differential is lower (30-50bp) and under the expectations that CNH will return to a discount to CNY, long USDCNH is more appealing at longer horizons.

Zero cost/small premium option structures can be devised (buy USDCNH call vs sell USDCNY call -equivalent topside strikes) to position for CNH returning to a discount to CNY. Risks are, namely,

1) The premium and 2) The CNH/CNY basis if spot trades above the topside strike.

Alternatively, we kept reiterating the ownership in a 1-year USDCNH seagull structure (USDCNH call spreads against selling a downside put strike) is appealing.