U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

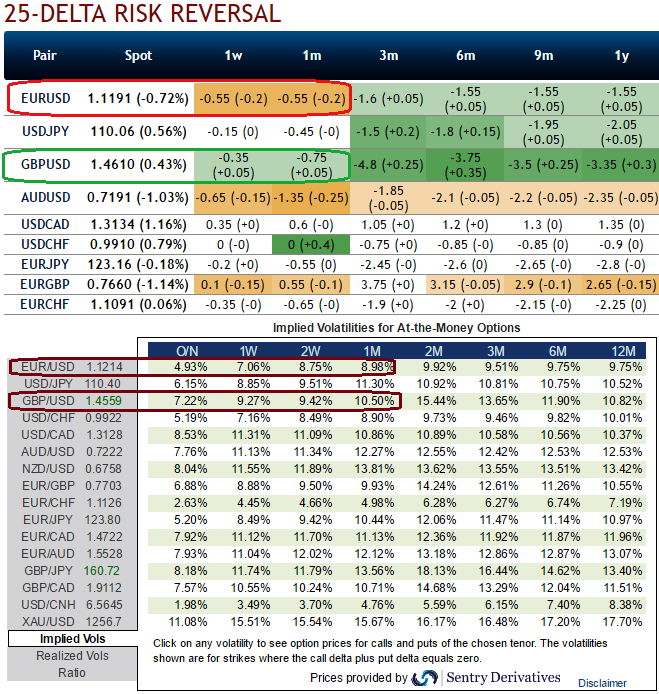

Before we begin with hedging framework let's once glance over OTC updates as to why do we prefer cross hedge between these pairs, we are particularly emphasizing on 1m risk reversals.

Please be noted that the risk reversals of EUR/USD of 1w to 1m tenors are signalling overpriced puts as they print negative flashes, while GBP/USD of 1w to 1m tenors signal positive to neutral hedging sentiments, as a result calls seem to be on higher demand.

The usual reason why cross-hedging happens is that because of the price difference or inability to find right derivative contracts on the same underlying whose risk needs to be hedged in any of the exchanges. Also this happens when the liquidity of these contracts is not really that great.

Well, let’s now visualize a trader decides after seeing above OTC nutshell for in the near month EUR/USD options that indicates overpriced ATM contracts; therefore he tends to short the volatility. And suppose we are shorting an ATM call option with an amount of 100,000 EUR. Currently, 1m IV of EURUSD and GBPUSD is 8.98% and 10.50% respectively.

If the delta is negative 0.5 since this is an ATM EURUSD put option, the amount would be -50,000 EUR in spot outright. To remove this potential risk taking place when the underlying market moves, we can buy 50,000 euro against dollar in the spot market anticipating euro to go up and take the same position in GBPUSD options as it was in GBPUSD.

This allows the delta neutral position. If prediction goes accurate then profit is certain by shorts on call option with nil risk as the market moves around as long as you continue to update the Delta hedge.

But always keep in mind that shorting an option in this case means returns are possible only when volatility falls.