Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

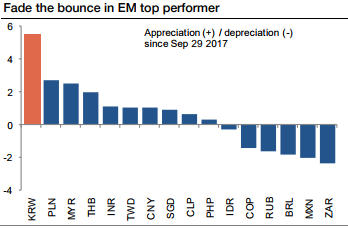

It seems that nothing can stop CNY and KRW, at least for now. KRW strengthened by another 0.2% versus USD this morning.

The rate hike expectation in South Korea has triggered the recent sell-off in USDKRW.

Some sort of dollar strength arisen lately but that was part of a broader turnaround in USD sentiment rather than anything KRW specific. Geopolitical issues have not ratcheted higher over this period but at the same time, the market remains wary that this could change quite quickly. This, in turn, leaves the market reluctant to chase USD/KRW lower.

As KRW accounts for 10% of China’s official CNY index, a rapid appreciation of KRW will translate into a lower USD-CNY exchange rate as the PBoC intends to stabilize the CNY-index.

However, even after past strong sessions, the CNY index has actually eased somewhat. In other words, if CNY fully tracks the KRW’s performance, USDCNY still has room to trend lower.

The G3 capex theme is a positive, as is the strength in China’s new economy (with the technology sector expanding strongly over the past 12 months). Korea is well placed to benefit from a continuation of these trends.

In fact, the Korean authorities think that KRW’s recent appreciation is overdone, warning that it will take actions to crack down the “excessive” activities.

However, it seems that nobody takes this seriously as traditionally the Bank of Korea is not an active player in the FX market. At the end of the day, the market cares about what you did, not what you said.

Risk-reward favors long dollar exposure from a short-term (1-2m) trading perspective. Large move relative to history and EM peers: The 5% KRW appreciation in the past two months represents a two-standard-deviation move (over a 2m period) since 2012 and the performance gap versus EM peers is very high.

Reversal after a large appreciation: In four episodes since 2012 when USDKRW has fallen by a similar magnitude as currently, the cross has subsequently corrected higher in three instances. Also, the BoK has been passive for most the year but could become more active in limiting downside given the speed of appreciation and peer outperformance.