Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

The stakes are high this week. A big shift in the trajectory of inflation in Australia would threaten both our view that the market will not move to price in hikes into the OIS strip, and that the AUD remains capped, with a range top at USD0.7850.

However, this is not our core view. A number of factors (rising under-employment, retail sector competition, and soft rental markets) all continue to suggest that we have not reached a significant point of inflection for core inflation. As such, the strategy into the number is to sell any strength in the AUD or any attempts to price in a tightening track for the RBA.

OTC Updates and hedging framework:

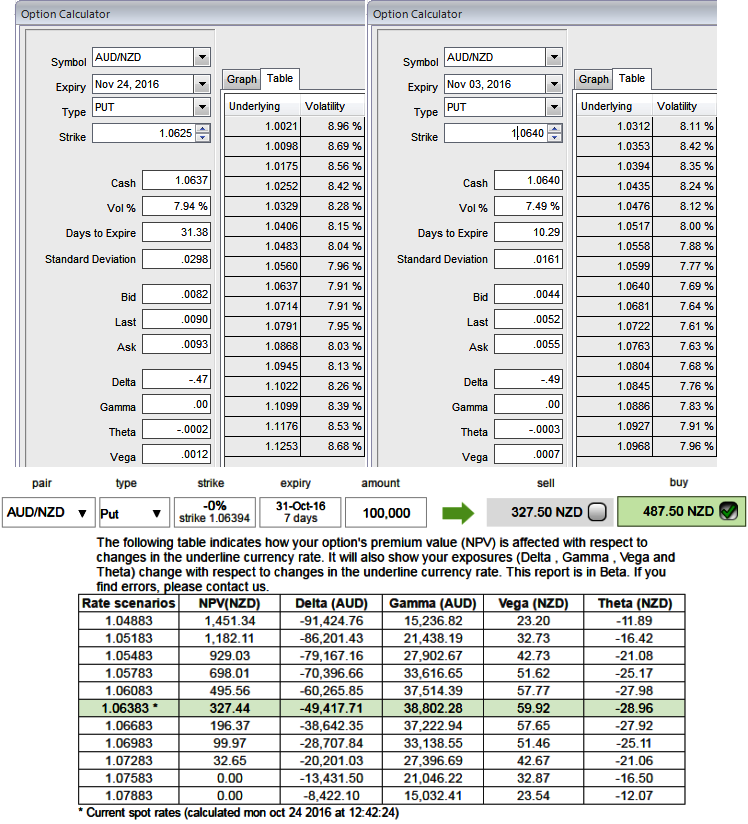

1W at the money volatilities of 50% delta calls and puts are hovering between 6.5% - 7.5% which is reasonable as the vols currently are working in the interest of option writers as you can see IVs and corresponding movements in vega.

Contemplating fundamental aspects and the current trend of this pair, the ATM IVs are creeping up at 7.94% and 7.49% of 1m and 1w tenors respectively that favor option writing rather than holding in short run.

While ATM puts are priced exorbitantly at 48% more than NPV, hence, we see a huge disparity between IVs and pricing. So, one can think of writing ITM puts with narrowed tenor combining ATM and OTM longs in put ratio back spreads.

The typical position combines buying at-the-money or out-of-the-money puts and, at the same time, selling a smaller number of in-the-money puts. Those in-the-money puts are always at risk of exercise, but you have two advantages.

First, the assignment can be covered by the long puts; second, time decay and implied volatility work in your favor on the short puts. This points out the importance of entering the position when implied volatility is higher than average.

The short position puts (which are in the money) will yield more premium income than the cost of the higher number of at- of out-of-the-money long positions. The ratio itself should vary depending on your belief in the strength, direction and timing of price movement, and also on the cost for each side. Creating a net credit is always desirable, so this also affects how many short and long puts you open.

Another issue is determining which strikes you should use in this strategy. The broader the strike difference between short and long puts, the fewer puts you need to sell to cover the price of the long puts. But at the same time, the coverage of long-to-short is going to be more difficult in the event of assignment.