U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Beyond the unwind of the earlier premium versus a heavily broadly discounted dollar as discussed earlier, the other major driver of the 7% trough-to-peak backup in USDCAD in 1Q was the divergence of policy pricing between the Fed and the BoC, wherein US-CA 2y swap spreads widened by as much as 28bps between early Feb and late March, which on our model would have been worth half of the 7% backup in USDCAD.

As with CAD risk premium as discussed above, there are other plausible reasons for a pricing in of a relatively more dovish BoC, including the run of negative data surprises in 1Q. But it is hard to divorce NAFTA risks from the BoC pricing outlook, particularly given that it has been part of BoC’s framework and rhetoric for the past year, particularly since October.

Meanwhile, despite recent data surprises, our economist have not changed their expectations for 4 BoC hikes this year, in-line with the Fed, given ongoing indications that inflation is at/above target and capacity is tight even in light of some near-term softening in activity.

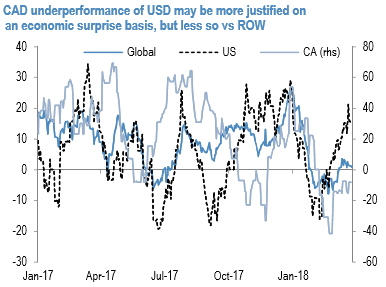

Finally, while the widening of US-CA rate spreads might be more justified given relative US-CA data surprises, the recent evolution in the data has been less differentiated versus rest-of-world economies, which again point to the recent relative underperformance of CAD on the crosses more compelling to fade (refer above chart).

We think there is medium-term value in fading the wide CAD underperformance and discount that has opened up recently versus peers, which in our baseline is not justified by relative monetary policy (4 BoC hikes this year), nor trade risk (no NAFTA crash-out). The potential near-term NAFTA break-through is a potential catalyst for the recent retracement of this underperformance to run significantly further. Therefore we buy CADJPY (bought at 85.195, stop at 83.0590) as a best risk-reward expression of CAD underperformance reversal.

FxWirePro launches Absolute Return Managed Program. For more details, visit: