Euro Retreats as Geopolitical Tensions Surge: EURUSD Eyes 1.1400 Floor Amid Safe-Haven Demand

Euro Retreats as Geopolitical Tensions Surge: EURUSD Eyes 1.1400 Floor Amid Safe-Haven Demand  FxWirePro: AUD/USD downside pressure builds, key support level in focus

FxWirePro: AUD/USD downside pressure builds, key support level in focus  FxWirePro: GBP/USD recovers but bears are not done yet again

FxWirePro: GBP/USD recovers but bears are not done yet again  FxWirePro- Woodies Pivot(Major)

FxWirePro- Woodies Pivot(Major)  FxWirePro: EUR/AUD eases slightly but trend is still bullish

FxWirePro: EUR/AUD eases slightly but trend is still bullish  FxWirePro- Major European Indices

FxWirePro- Major European Indices  FxWirePro: GBP/USD outlook weaker on renewed downside pressure

FxWirePro: GBP/USD outlook weaker on renewed downside pressure  FxWirePro:NZD/USD drifts lower, could be on verge of bigger drop

FxWirePro:NZD/USD drifts lower, could be on verge of bigger drop  FxWirePro: USD/ZAR sustains gains as uptrend remains strong

FxWirePro: USD/ZAR sustains gains as uptrend remains strong  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  EUR/JPY Bulls Charge: Eyeing 186.00 as Euro Strength Intensifies

EUR/JPY Bulls Charge: Eyeing 186.00 as Euro Strength Intensifies  FxWirePro: EUR/AUD gaining momentum for a move towards 1.6800 level

FxWirePro: EUR/AUD gaining momentum for a move towards 1.6800 level  Bitcoin Battles Volatility: Institutional Support Eyes USD 64,000 Floor Amid Geopolitical Tensions

Bitcoin Battles Volatility: Institutional Support Eyes USD 64,000 Floor Amid Geopolitical Tensions  Ethereum Retreats Toward USD 2,000: Technicals Signal Caution as ETH Mimics Bitcoin’s Pullback

Ethereum Retreats Toward USD 2,000: Technicals Signal Caution as ETH Mimics Bitcoin’s Pullback  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary

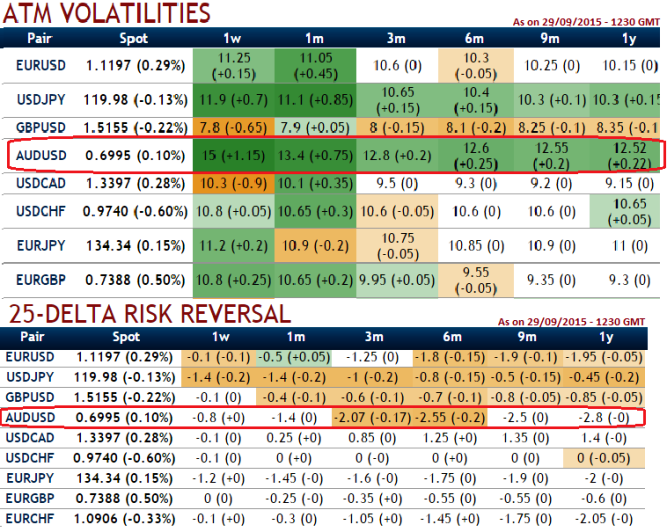

With spot FX flashes of AUDUSD at 0.6995 we see delta risk reversal for 1 week contracts have shown slight recovery signals but long term (1M-1Y) put contracts are on higher demand. As you can make out from the nutshell showing AUDUSD still maintains the highest implied volatility of 1W at the money contracts among G20 currency pool, almost at 15%.

As a reminder, this higher IV represents how much movement today's FX market expects from AUDUSD during US sessions and the life span of the option. In that respect, an option buyer is partially buying the market's expectations for this pair.

Comparing these two factors and synthesizing while projecting the trend we understood the following fact. In foreign exchange (FX) market prices move to extremes more frequently and these extreme levels is referred to as "Fat Tails". If more price actions occur at the fat tails, the option trader will mark volatility higher for out-of-money (OTM) and in-the-money (ITM) options then at-the-money (ATM) options and so does happen with AUDUSD pair currently. If there is no downside bias in market expectations of the underlying price then the price of volatility is symmetrical around ATM options.

AUD/USD Put Ratio Back Spread:

One can now set up AUDUSD put ratio back spread regardless of upswings by improving odds in its positions as explained below. That In-The-Money puts on short side in put ratio back-spreads are always at risk of exercise if the market tumbles, but you have two advantages.

Firstly, keeping maximum tenor on long side: Giving a longer time to expiration for long sides, any abrupt drastic moves on the downside so that assignment can be covered by the long puts. Secondly, time decay advantage: Using near month contracts or contracts shorter tenor on short side signifies the importance of entering the position when IV is lower than average but AUDJPY IV is seen at 10% which is quite higher side (due to data season), so let us keep maturity on short side as normal as near month contract period. Time decay and implied volatility work in your favor on the short puts.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Buy AUD/USD risk reversal on higher IV – PRBS for hedging

Wednesday, September 30, 2015 7:11 AM UTC

Editor's Picks

- Market Data

Most Popular