China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why

Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence

Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150

The Bank of Japan left its key short-term interest rate unchanged at -0.1% at its March 2018 meeting, as widely expected to be on hold. While the bank will be encouraged by 2017’s growth result, core inflation is still below target at 0.9%. Policymakers also kept its 10-year government bond yield target around zero percent and maintained its upbeat economic view ahead of a new term for Governor Haruhiko Kuroda.

JPY somewhat underperformed in G10 and especially with USD amid firm risk sentiments until early February, and then turned to outperformer, triggered by a plunge in global stocks. On net, as the latter was more dominant, JPY became the outperformer within the G10 camp during the relevant period.

On the flip side, NZD was the worst performing G10 currency vs USD in 2017(refer above chart). A combination of weaker-than-expected economic growth, tighter funding conditions, slowing net immigration and a change of government all conspired to relegate NZD to wooden spoon territory last year.

We don’t think many of these factors will be too different in 2018, and so still see scope for underperformance from NZD in the year ahead.

We foresee that NZDJPY to breach recent ranges to the downside in 1H’18 and forecast the currency at JPY 75.153 by mid-2018. From there, it is reckoned that the currency should settle at USD 72.427 levels by the year-end.

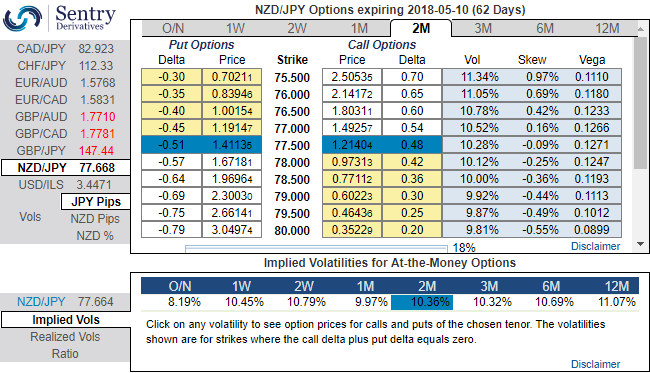

ATM IVs of NZDJPY is trending above 10.30% for 2m tenors and positively skewed IVs of these tenors are evidencing bearish hedging interests. Bids for OTM puts upto 75.50 is noticeable to signify the downside risks which is almost in line with our above-stated projections.

Accordingly, conservative hedgers can prefer the below strategy:

Debit Put Spread = Go long 2M ATM -0.49 delta Put + Short 2m (1%) OTM Put with lower Strike Price with net delta should be at -0.16. Please be noted that the positive payoff structure would be generated as it keeps dipping below current levels but remain within OT strikes.

For a net debit, bear put spread reduces the cost of trade by the premium collected (on the shorts of OTM put) and keeps option trader to participate in downward moves and any upswings in abrupt.

Moreover, the risk is capped to the extent of initial premium paid, as opposed to unlimited risk when short selling the underlying outright.

However, put options have a limited lifespan. If the underlying FX price does not move below the strike price before the option expiration date, the put option will expire worthless.

A more muted dollar environment should also tilt USD-correlations lower. Express a soft bearish USD correlation via option triangles that sell USDJPY and NZDUSD puts hedged with long NZDJPY puts.

Currency Strength Index: FxWirePro's hourly NZD spot index is displaying shy above 46 levels (bullish), while hourly JPY spot index was at -52 (bearish) while articulating (at 11:02 GMT). For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex

FxWirePro launches Absolute Return Managed Program. For more details, visit: