Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

The US Federal Reserve maintained monetary policy unchanged last night, as broadly anticipated. The accompanying statement was a little more upbeat than before, noting the improvement in consumer and business sentiment. Importantly, though, there was no strong signal of a near-term hike. Domestically, the House of Commons voted to provide the government the ability to trigger Article 50 to start EU withdrawal negotiations by the end of March.

The Bank of England unanimously announces no change in policy today, leaving rates at 0.25% and the planned total stock of asset purchases at £445bn, and maintain the ‘neutral’ bias adopted in the November Inflation Report.

Notably, Governor Carney’s speech on 16 January repeated that monetary policy can respond “in either direction”, with the MPC for the moment choosing to tolerate a period of rising inflation. The data continue to bear out the UK economy’s post-referendum resilience, while further rises in inflation are coming down the tracks.

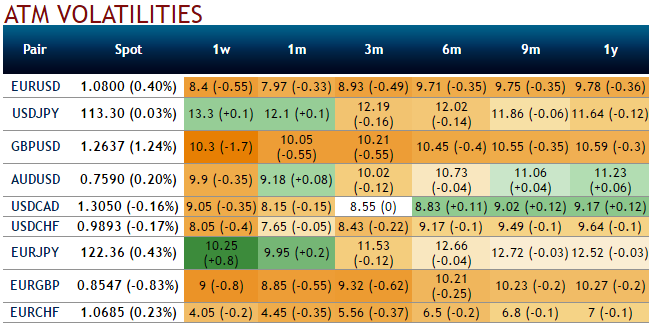

The UK would pursue a different future outside Europe, but the removal of uncertainty around the British stance should prove bearish for GBP volatility. Please be noted that the IVs of GBP crosses (especially EURGBP) has been reducing despite series data, such as the UK PMIs, BoE monetary policy. Accordingly, we’ve devised below option strategy.

Option-trade recommendations: (Writing a strangle)

For those whose foresee non-directional that is existed in this pair from the last couple of months or so to prolong in reducing IV scenario, prefer to remain in the safe zone, we recommend shorting a straddle considering IV shrinks.

Thereby, one can benefit from certain returns by shorting both calls and puts.

Thus, short 7D (0.5% OTM striking) put and (0.5% OTM striking) call simultaneously of the same expiry (preferably, short term for maturity is desired).

The strategy is likely to derive the maximum returns as long as the underlying EURGBP spot FX price on expiry keeps trading between 0.85 and 0.86 levels only as both the instruments have to wipe off worthless. So that the options trader gets to keep the entire initial credit taken as profit.