Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

NZD faces headwinds, even in a clearly weak USD environment. Domestic growth has weakened, the central bank’s inflation forecasts have been revised materially lower, net immigration is slowing and business confidence has fallen significantly since the change of government. But with the central bank in a state of transition (new governor, new mandate), over the next couple of months, we don’t see any domestic monetary policy catalysts that would drive material NZD weakness in the near-term.

Over 2018, we see scope for underperformance from NZD, though this is now more contingent on ongoing confirmation that the RBNZ can credibly lag policy normalization in the G3, and perhaps on evidence that real assets (equities, housing) are threatened by late cycle growth dynamics and government intervention.

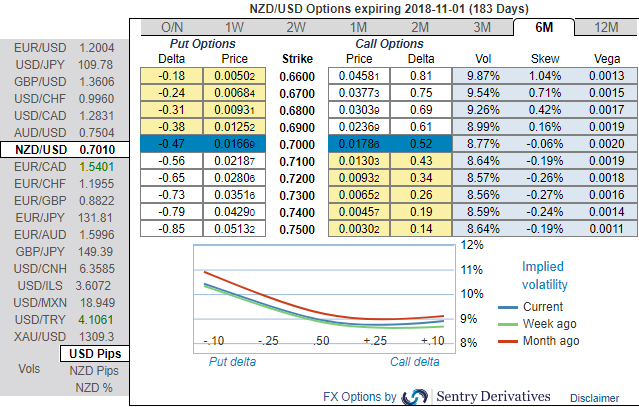

Bids on 3m skews have come in quite worthy, as they signaled the hedging interests bearish risks. Thus, we expect NZDUSD to depreciate to USD0.68 by end of 3Q’19. Accordingly, we’ve recommended diagonal put ratio back spreads in order to participate both momentary upswings in the consolidation phase and anticipated downside risks.

Writing 1m (1%) in the money put with positive theta snaps decisive rallies, you could easily make out short legs on ITM puts would go worthless considering time decay advantage. Simultaneously, we uphold 2 lots of longs in 3m 1% OTM puts, the structure could be constructed either at net debit.

It was explicitly stated that “Theta shorts are recommended in this strategy because, Theta is not a constant, it changes as the underlying market moves and time passes. Theta is the sensitivity of an option’s value to the passage of time. It is usually expressed as the change in value per one day’s passage of time.”

Well, for now, the medium term perspectives of this pair seems to be bearish as the US dollar remains in a two-month-old sideways range, which means further sideways ranging in NZDUSD is possible during the month ahead.

Further out, though, we are bearish. The NZ-US interest rate advantage is rapidly shrinking and should eventually weigh, pushing NZDUSD towards 0.68 by mid-year.

Moreover, the 6m skews are targeting towards OTM put strikes at 0.66 (refer above nutshell) which is in line with the above-mentioned projections.

Hence, on hedging grounds, the option the holder of OTM puts still desirable and is deemed to be on upper hand.

Currency Strength Index: FxWirePro's hourly NZD spot index is inching towards -4 levels (neutral), while hourly USD spot index was at shy above 97 (bullish) while articulating at 05:48 GMT. For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex.

FxWirePro launches Absolute Return Managed Program. For more details, visit: