EURJPY Bounce Loses Steam Below 184 — Sell-the-Rally Setup Eyes 183 Target

EURJPY Bounce Loses Steam Below 184 — Sell-the-Rally Setup Eyes 183 Target  FxWirePro: GBP/USD heads deeper into bear territory, 23.6% fibonacci eyed

FxWirePro: GBP/USD heads deeper into bear territory, 23.6% fibonacci eyed  FxWirePro:NZD/USD rout continues without relief

FxWirePro:NZD/USD rout continues without relief  AUDJPY Bears Take a Breather at 111.50, But ‘Sell on Rallies’ Still Eyes 110

AUDJPY Bears Take a Breather at 111.50, But ‘Sell on Rallies’ Still Eyes 110  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro: USD/CAD uptrend loses steam, remains on bullish path

FxWirePro: USD/CAD uptrend loses steam, remains on bullish path  FxWirePro : AUD/USD drifts lower, could be on verge of bigger drop

FxWirePro : AUD/USD drifts lower, could be on verge of bigger drop  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  FxWirePro:GBP/USD recovers slightly from early decline but bears are not done yet

FxWirePro:GBP/USD recovers slightly from early decline but bears are not done yet  FxWirePro: AUD/USD drifts lower, uninspired by jobs beat

FxWirePro: AUD/USD drifts lower, uninspired by jobs beat  FxWirePro: NZD/USD extends losing run, eyes 0.5600 level

FxWirePro: NZD/USD extends losing run, eyes 0.5600 level  BTC Slips Below $60K as Institutional Demand Dries Up — Bears Eye $59K Support, Rallies to $63K for Shorts

BTC Slips Below $60K as Institutional Demand Dries Up — Bears Eye $59K Support, Rallies to $63K for Shorts  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary

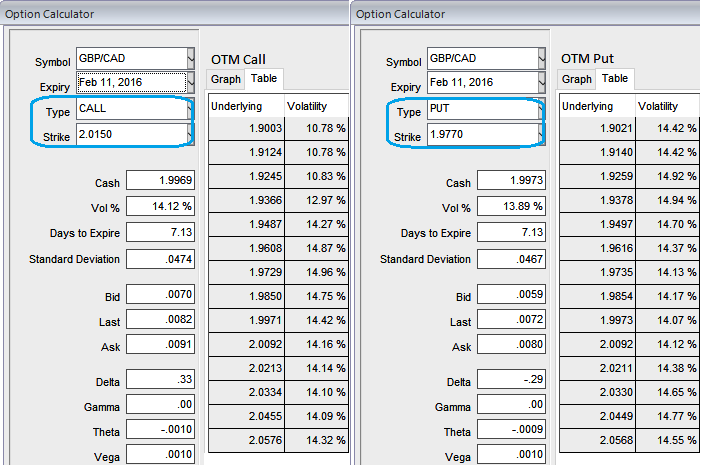

We would say GBPCAD likely to evidence some corrections but if you think that GBP should revert to outperformance on the crosses or you are in love with GBPCAD's uptrend or stuck with any payable exposure, now worries we have a customized hedging arrangement, while 1M ATM volatilities remain higher at 12.08%, then cover your underlying currency exposures with collars strategy exclusively on hedging grounds.

Further into 2016, there are two key risks for GBP - the UK's unsustainable current account deficit and the EU referendum, promised for end-2017 at the latest. Not only that, so long as the government's strategy to reduce the budget deficit remains credible, the deficits (internal and external) should remain fundable, but it is increasingly the case that rate hikes are required to stop downside risks to GBP crystalizing. As to the rising risk of UK EU exit, on the face of it, there are reasons to think GBP should carry a rising risk premium.

Technical glimpse: Currently, the pair is struggling at 1.9950 with more selling pressures boiling, in our opinion it seems unlikely to hold this level even during US sessions then there would certainly be a steep dips on daily charts which is to be treated as more booster for continuation of downtrend with leading oscillators are showing downward convergence with the price dips. RSI (14) on intraday terms approached oversold zones and still converging with every price declines, while prevailing prices have slid below 21DMA that signifies downtrend to prolong in the days to come.

Hedging Strategy: The strategy is constructed for those who have spot FX Euro exposure at present who are concerned about a correction and wish to hedge the long spot currency position, Write deep (1%) OTM call option + hold an (-1%) OTM put option (near month Call & mid-month put). This helps as a means to hedge a long position in the underlying outrights by holding longs on protective put.

The gamma of the collar spreads is the summation of position adjusted gammas of its component option instruments. Gamma of both OTM call strike (2.0150) and OTM put strike (1.9770) have been zero. So, Gamma of collar spread which would again be closer zero. Gamma of the option is mainly dependent on the moneyness of the option. Well, when you are shorting OTM call with positive theta this is a good news for writers.

Thereby, the maximum return = Strike price of call - Currency spot price - net premium paid or Strike price of call - Currency spot price + net credit received on short side. Remember again, this is purely for hedging; speculators should stay away from this strategy.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Adamant bulls in GBP/CAD can hedge unsustainable rallies with collar gamma combinations

Thursday, February 4, 2016 12:09 PM UTC

Editor's Picks

- Market Data

Most Popular