Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

In our recent post, we shed light on lower FX vols, where stated FX vols have been perplexingly soft over the past two weeks in the face of escalating trade war rhetoric and equity markets’ jitters have been the talking point de jour in FX option circles. While it was also stated ATM implied volatilities of G10 FX universe which are at its least, almost across all the tenors, IVs have been shrinking amid trade clashes between the US and China.

In this write-up, we emphasize on why inertness in FX vols that we have encountered are largely unsatisfying; we list some of them and a couple of our own below:

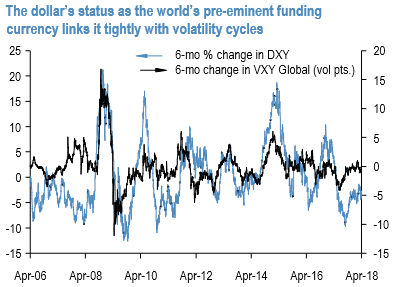

The simple stand perhaps the most compelling is the direction of the dollar. The dollar’s status as the world’s pre-eminent funding currency that seeks out high return international investments during economic expansions and retreats home in crises has led to a tight correlation between USD and FX volatility cycles over the past two decades (refer above chart).

It seems challenging for the universe of dollar-funded balance sheets to absolutely unwound, so goes the argument, as long as a weaker US currency remains a key component of the Trump administration’s efforts to reconfigure the global trade/FX architecture and investors concurrently anticipate widening twin deficits to lead to further dollar slippage. Even so-called fragile EMs like Turkey with wide current account deficits that require financing can get a stay of execution from stock market weakness in this climate as long as portfolio flows are inward bound, not the reverse.

Since the dollar has been largely range-bound for the past two months and has actually bounced 2% from its late March lows, the weak dollar rationale does not strictly explain the very recent past. A second explanation, this one behavioral, is that two months of placidity in the weak dollar trend is testing the resolve of investors to remain in the two major short USD trades of the year-long Euro and long Yen –both of which now incur substantial negative carry on points.

By extension, high theta on option-based expressions. The first step in investor risk forbearance is to avoid buying i.e. a drying up of the USD put demand of January. The second is de-risking which involves active option liquidation; subjective accounts suggest that this has so far happened at the edges, and more could be in store particularly in the yen which IMM positions data shows has been almost entirely short-covered since the turn of the year. The investor performance context is important too: global macro hedge funds with a +5% P/L kitty by end-January (basis HFR Macro/CTA index) had pain thresholds to withstand some volatility around core views that have been revised significantly lower with YTD P/L of-2%.

FxWirePro launches Absolute Return Managed Program. For more details, visit: