BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence

Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

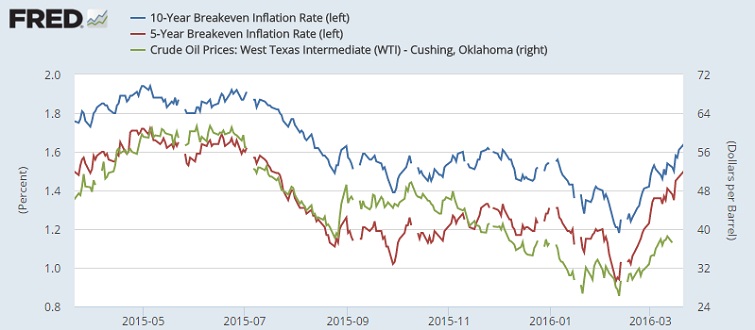

Breakeven inflation rates in United States and around the world are rising, with partial thanks to higher oil price. However, there is probably more to infer from this rising expectations rather than just to consider it as offshoot effects of recent rise in oil price.

- From recent rise in inflation expectations, which rose by 46 basis points since February it is quite evident that oil price is losing intensity of its impact over inflation expectations. That is right to be the case due to lower base effects. Going forward it is more likely that US inflation expectations will rise even if oil stabilizes at current levels. Core consumer inflation, which excludes fuel and food, already breached FED’s 2% target and hovering at 2.3%.

- As of now, 10 year break even inflation is hovering at 1.65%, while 5 year breakeven is at 1.5%. These rates are at highest since summer of 2015.

- Moreover, from the global breakeven inflation rates, we can infer that impact of oil over inflation is not similar to everywhere. In US 60 day rolling correlation between Crude and inflation expectations stand at 55%, whereas it is just 30% for Europe (taking Germany as benchmark).

So, US economy will be more prone to rate hikes, if oil rises from further, whereas Europe will need contributions from beyond oil to boost inflation.