Bank of Japan Signals Readiness for Near-Term Rate Hike as Inflation Nears Target

Bank of Japan Signals Readiness for Near-Term Rate Hike as Inflation Nears Target  Japanese Pharmaceutical Stocks Slide as TrumpRx.gov Launch Sparks Market Concerns

Japanese Pharmaceutical Stocks Slide as TrumpRx.gov Launch Sparks Market Concerns  Trump Endorses Japan’s Sanae Takaichi Ahead of Crucial Election Amid Market and China Tensions

Trump Endorses Japan’s Sanae Takaichi Ahead of Crucial Election Amid Market and China Tensions  Global Markets Slide as AI, Crypto, and Precious Metals Face Heightened Volatility

Global Markets Slide as AI, Crypto, and Precious Metals Face Heightened Volatility  Gold Prices Slide Below $5,000 as Strong Dollar and Central Bank Outlook Weigh on Metals

Gold Prices Slide Below $5,000 as Strong Dollar and Central Bank Outlook Weigh on Metals  Gold and Silver Prices Rebound After Volatile Week Triggered by Fed Nomination

Gold and Silver Prices Rebound After Volatile Week Triggered by Fed Nomination  Dow Hits 50,000 as U.S. Stocks Stage Strong Rebound Amid AI Volatility

Dow Hits 50,000 as U.S. Stocks Stage Strong Rebound Amid AI Volatility  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  South Korea Assures U.S. on Trade Deal Commitments Amid Tariff Concerns

South Korea Assures U.S. on Trade Deal Commitments Amid Tariff Concerns

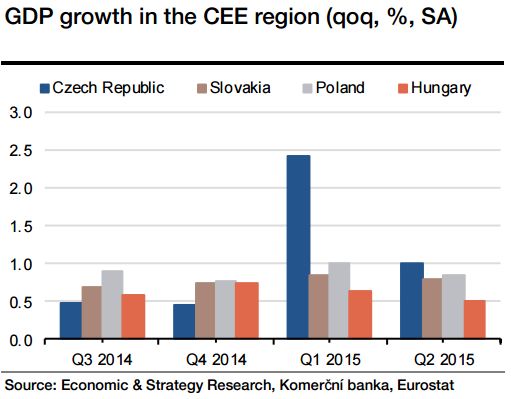

The structure of GDP growth in the Centeral and Eastern Europe (CEE) region is gradually changing. While in 2011 and 2012, net exports represented the key source of GDP growth, we are now seeing a visible shift towards domestic demand. This is important as it reduces the region's reliance on the external environment as well as its exposure to macro-economic risks (slowdown in China, Grexit scenario and geopolitical risks).

Domestic demand has now become the key driver of GDP growth, particularly in Poland, Czech Republic and Slovakia, while net exports are tending to reduce growth or support it just marginally (in Q2 15 net exports contributed 0.1pp yoy to GDP growth in Poland and 0.3pp yoy in the Czech Republic). A different situation can be seen in Hungary, where net exports continue to play an important role in the country's economic performance (in Q2 15 net exports contributed 1.5pp yoy to growth). For the CEE region as a whole, we expect this trend to continue as rising domestic demand is likely to put upward pressure on imports of investment and consumer goods, while exports could suffer from the still weak euro-area revival.

Household consumption and fixed investment are thus gradually taking over as the key GDP growth drivers in the CEE region, while government consumption is pushing growth higher as well. Household consumption is being supported by rising employment across the region, rising wages and increasing household spending appetites. Fixed investment is also showing strong growth as CEE governments try to tap as much money as possible from the EU funds as the chance to obtain funds for the programming period 2007-2013 ends this year. Gross fixed capital formation increased by more than 6% yoy on average within the CEE countries, with Slovakia at the top (9.4 % yoy). From the supply-side point of view, manufacturing and the wholesale and retail trade remain the key drivers of GDP growth in the region. Nevertheless, growth is fairly evenly spread across most sectors (although significant drops have been observed in the Hungarian agricultural sector and the Slovak financial sector).

Next year, the new 2014-2020 programming period for tapping EU funds will start. This usually leads national governments to make less of an effort to pump money. As a result, fixed investment is likely to decelerate next year and the region's GDP growth will subside. For the Czech Republic, we expect GDP to grow by 4.5% this year, but to slow down to 2.7% next year due to the drop in EU-fund related investment. Meanwhile, the Polish and Slovak economies should remain above 3% while Hungarian GDP is likely to decelerate from 3.3% this year to 2.5% in 2016, according to the Hungarian central bank.