Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’  Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season

Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150

The ECB clearly disappointed markets on several fronts with its bare-minimum easing package. The decision though not unanimous was taken by a "very large majority". ECB may have under delivered but delivered nonetheless. The elements announced were as follows:

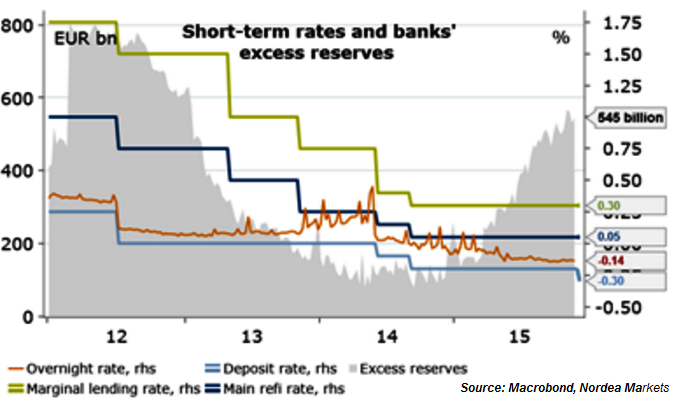

A lower deposit rate (-10bp to -0.3%), Asset purchases will be extended until the end of March 2017 or longer, Inclusion of local and regional government debt in EUR, Principal payments will be reinvested, Full allotment procedure in refinancing operation will be continued at least until the end of 2017.

The ECB action sent Euro shorts scrambling for cover, bond yields spiked and equities were sent into a tailspin. It was obviously not all that the ECB would do at this point. The ECB definitely still has an easing bias. The message from the ECB is that very easy monetary policy will be around for a very long time. Draghi also stressed the flexibility of the asset purchase programme.

The policy rate corridor is now asymmetric with the marginal lending rate 25 bp above the main refi rate and the deposit rate 35 bp below. The practical relevance is limited as overnight money is trading closer to the deposit rate because of excess liquidity.

"The overall purchase volume in the QE programme will rise from EUR 1,140 bn to EUR 1,500 bn or by almost one third or 3½% of GDP. While not insignificant, it's not a whole new world, especially as few were expecting the purchases to end next year. In fact, we find it unlikely they could buy EUR 60bn in one month and nothing the next, so eventually a tapering process will be needed", says Nordea Markets Research.

The biggest reason why the ECB did not do more was probably attributable to recent rebound in inflation expectations despite continued fall in oil prices, which Draghi also noted. Now, if the rebound in inflation expectations is not sustainable, the ECB could quickly find itself in a position of needing to do more.

"Based on Draghi's message, a further cut in the deposit rate would probably be the easiest next step for the ECB, while an increase in the monthly pace of the purchases would be a bigger step. The ECB wants to keep all doors open", adds Nordea.

A massive EUR shorts squeeze on Thursday pushed the Euro to 1.0981 against the Greenback, the biggest one-day surge in the pair in nearly seven years. EUR bulls faced some exhaustion in Asia, after witnessing almost 450 pips rally in the previous session. The pair is trading at 1.0884 as of 1155 GMT. More volatility likely as markets now brace for the US non-farm payrolls data due in the NY session.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Does the ECB still have an easing bias?

Friday, December 4, 2015 12:33 PM UTC

Editor's Picks

- Market Data

Most Popular