RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Oil Prices Slip as Iran Talks and Strong Supply Outlook Ease Market Concerns

Oil Prices Slip as Iran Talks and Strong Supply Outlook Ease Market Concerns  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Trump Administration Declines USMCA Renewal, Opens Talks on New Trade Changes

Trump Administration Declines USMCA Renewal, Opens Talks on New Trade Changes  US Resumes Dollar Shipments to Iraq After Months-Long Suspension

US Resumes Dollar Shipments to Iraq After Months-Long Suspension  Turkey Vehicle Sales Fall 11.4% in June as Auto Market Weakens

Turkey Vehicle Sales Fall 11.4% in June as Auto Market Weakens  US Jobs Report Preview: June Payroll Growth Seen Slowing as Fed Rate Decision Looms

US Jobs Report Preview: June Payroll Growth Seen Slowing as Fed Rate Decision Looms

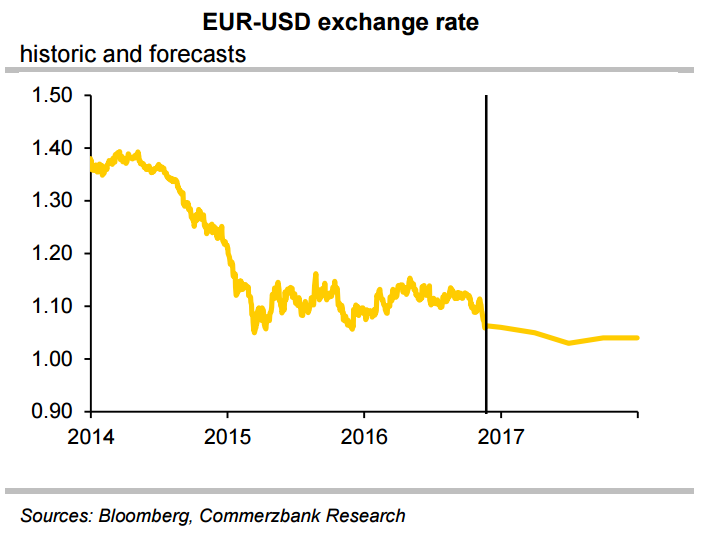

The European Central Bank (ECB) will decide on December 8 on whether and how to extend its 80 billion euros ($85 billion) monthly bond purchases and expectations are for the programme to continue beyond its current March deadline. Two of the top officials said earlier this week that the ECB needs to continue supporting the euro zone economy with its ultra-loose policy, cementing expectations for an extension of the ECB's bond-buying scheme next month.

Euro zone inflation was 0.5 percent last month and is expected to rise beyond 1 percent early next year, mainly due to a stabilisation in oil prices. However, the ECB is still a long way off its inflation target of almost 2 percent.

Analysts are not very hopeful that the economic environment or the core inflation trend in the eurozone will improve notably. President Mario Draghi also told a European Parliament committee on Monday the ECB needed to maintain its current level of monetary support to bring euro zone inflation back to its target.

"The ECB will be forced to get active again and will prolong the deadline of the asset purchases beyond March 2017 for another six months. Our experts do not expect another cut of the deposit rate, though," said Commerzbank in a report.

The US economy rose by a solid 2.9 percent q/q (annualised) in Q3 and the unemployment rate is lingering at 5 percent. Inflation stood at 1.5 percent y/y and the Fed’s preferred mean for core inflation, the PCE index, at 1.7 percent. Based on improving fundamentals, the Fed signalled an imminent rate hike at its October meeting. At its November meeting, he Fed refrained from hiking the key rate ahead of US presidential election on 8th November, but repeated the strong indication for a hike.

Donald Trump' victory has raised US interest rate expectations markedly. Trump's expansionary fiscal and protectionist trading policy are likely to boost the USD and drive up inflation. A rate hike in December is now almost fully priced in by markets. The market has also come to attach a likelihood of over 50 percent to two additional Fed rate hikes in 2017.

Fed will keep hiking interest rates whereas the ECB will stick to its expansionary stance. With Fed and ECB monetary policies diverging further, EUR/USD is likely to remain subdued. By end-2017 the ECB will be forced to gradually stop buying bonds as it will gradually run out of eligible assets. This should support the euro against the US dollar by the end of 2017.

EUR/USD was trading at 1.0620 at around 1210 GMT as markets await FOMC minutes due later in the NY session. At the same time, FxWirePro's Hourly USD Spot Index was at 32.9119 (Neutral) and Hourly EUR Spot Index was at 69.1643 (Neutral). For more details on FxWirePro's Currency Strength Index, visit http://www.fxwirepro.com/currencyindex