Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone

Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Morgan Stanley Names Marks & Spencer Top European Retail Pick, Sees Strong Upside

Morgan Stanley Names Marks & Spencer Top European Retail Pick, Sees Strong Upside  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook

Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Bitcoin spiked higher in June but for now, struggling for the momentum, surged from $9,049 to the recent highs of $13,200 levels. While bears plummet below 7 & 21-DMAs, consequently, the pair slid below $10.5k. Both leading indicators signal overbought momentum that indicates the selling sentiments and lagging indicators still edgy.

Technically, after BTCUSD has bottomed out at $3,122.28 levels, the bullish engulfing pattern has occurred at $4,071.70 levels, consequently, surged to the June highs of $13,880 levels which is almost more than 344% so far (in just 6-7 months or so) (refer monthly chart). The pair has been trading on a sideways market on an intraday trading basis. The horizontal channels that are acting as the pair’s price resistance level $10694.22 and support level $10374.41 that confirmed the sideways trend.

After peaking at the end of June, Bitcoin has been struggling in July raising questions about overbought conditions.

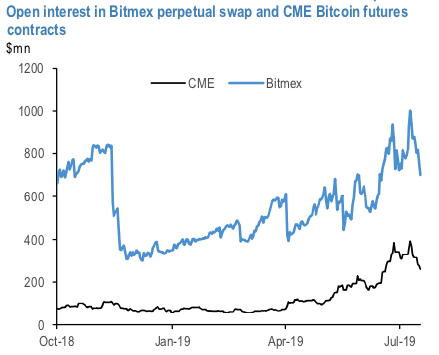

To address this question, we resort to futures contracts and in particular, the two most important Bitcoin futures contracts: the CME futures contract and the less regulated perpetual swap contract traded at Bitmex. Both of these contracts are mostly driven by institutional investors. We argued before that the relative importance of institutional investors has structurally risen for the Bitcoin market over the past year as the previous cryptocurrency bubble of 2017 collapsed during last year, inducing many retail investors to exit the market.

How big are the above contracts? The 1st chart depicts the open interest of these two contracts. The open interest is more than double at Bitmex (around $700mn currently vs around $300mn for CME) which reflects the success of the Bitmex contract in concentrating liquidity over the years, by starting earlier and by allowing investors to lever a lot more than CME for up to 100x. Average weighted leverage is admittedly lower than that, around 25x, but still ten times higher than the 2.5x allowed by CME.

So accounting for the differences in leverage, the actual capital committed (which is a function of the open interest divided by leverage) by participants at CME futures is much bigger, perhaps four times bigger than the capital committed by participants at Bitmex (even as the open interest of the later is more than double).

In addition, the CME contract has been exhibiting strong momentum recently, making new records over the past quarter in terms of open interest, volumes, and investor participation:

Q2 2019 was the strongest quarter to date with the average daily volume of 10,710 contracts (53,550 equivalent bitcoin; $403MM), almost 200% greater than Q2 2018;

Greatest Open Interest – 6,069 contracts – June 26th(30,345 equivalent bitcoin; $385MM);

The highest number of Large Open Interest Holders (a LOIH is any entity that holds at least 25 BTC contracts), 49 as of June 25th;

751 new unique accounts added in Q2, most added in any quarter; 34% growth from Q1 2019; and

Over 1,070 accounts actively traded in June, the highest number observed in any month and 40% more than the active accounts in May.

Given the regulatory advantage of CME relative to Bitmex, we expect that strong CME momentum to continue.

The open interest proxy is shown in the 2nd chart for both CME and Bitmex contracts. Both proxies show that Bitcoin got rather overbought at the end of June. And while some of this previous overhang of crowded long Bitcoin futures positions unwound in July, more unwinding is likely needed to push Bitcoin to neutral or oversold territory. Until that happens, Bitcoin will likely continue to struggle to maintain the previous months’ gains. Courtesy: JPM