Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Chinese stock market is the most volatile in the world. At the peak of the crash, 5 day average of realized volatility reached close to 10% for its benchmark stock index Shanghai Composite. It has fallen substantially over intervention but still around 4%, still high compared to global standard

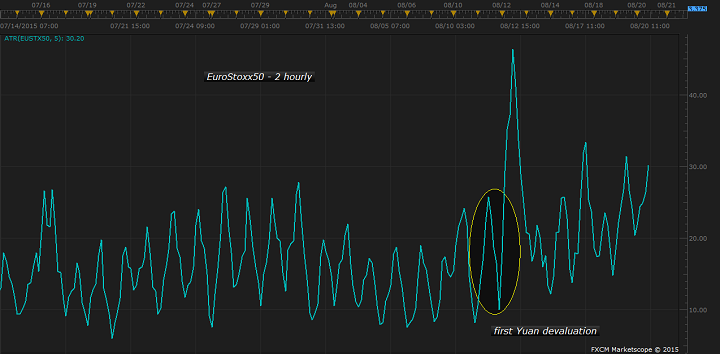

In a bid to better manage its currency, Chinese central bank devalued Yuan resulting in a spill-over of volatility across global market, especially in European equity markets.

- Emerging market currencies along with mining stocks are being hammered all across globe, as fear is rising for hard landing in China. China might be weaker than many had originally assumed and there is a growing risks that in spite of denial by People's bank of China (PBoC), there could be further devaluation even market driven one.

- Chinese devaluation of Yuan for three consecutive days last week, clouded monetary policy and its effect from European Central Bank (ECB) and raised the risk of currency war.

European blue chip index, EuroStxx50 registered substantial rise in volatility. 5 day average of realized volatility has almost doubled, both daily and intraday.

5 day average of daily realized volatility is up from around 1% before intervention to 1.8% as of today and 2 hourly volatility jumped from 0.5% to 0.9%, while the index lost about 8.5% since the intervention.