USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone

Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher

Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher  Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

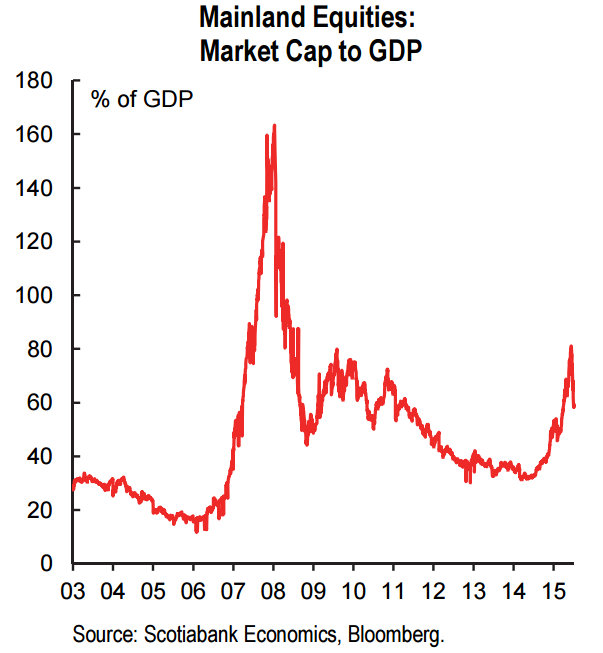

Volatility in the Chinese markets could be far from over. China's Mainland equities fell over 32% after peaking on June 12 despite a myriad of measures implemented by policymakers to halt the correction.

The sharp fall in Chinese equities has started to send shock waves through broader markets. There is a growing fear that the Chinese stock market correction will produce serious knock-on effects that hamper broader growth. The largest direct negative effect of a pronounced stock market decline will be a slowdown in IPO activity. However, Scotiabank opines that equity issuance remains only a small part of financing in China worth about 5% of aggregate financing, and doubts corporate finance will be meaningfully derailed.

"The equity market correction will have only modestly negative and short-lived effects on the real economy, and so does not represent hard landing material", says Scotiabank in a report.

Financial intermediation remains a small share of the economy at about a 6 percentage point weight in Chinese GDP, and there is a little evidence of meaningful linkages between GDP in the financial intermediation sector and volume measures of stock market activity.

"We are not unconcerned about the macroeconomic effects of correcting Chinese equity markets but not sufficiently worried to view it as hard landing material versus a relatively minor and short-lived drag on economic growth and financial stability", adds Scotiabank.

China's foreign trade improved in June with exports rising for the first time since March and the contraction in imports narrowing. Both results were above market expectations. Imports of major commodities rebounded following a weak May. The volume crude oil imports were 7.2mb/d in June, up 26.7% y/y.

"We expect better export and import growth in Q3, but from low levels. External demand should improve, as suggested by better US and euro area data. More importantly, we believe domestic economic activity is finding a floor in Q3, and the negative price effect on imports, in place since H2 14, should start to fade, supporting a smaller contraction in imports. Overall, we expect a current account surplus of 2.9% of GDP for the full year, up from 2.1% of GDP in 2014" estimates Barclays Capital in a report today.

Commodity currencies will be most vulnerable should the Chinese equities rout extend. China's stock market and related policy developments will be more closely monitored by markets.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Chinese equity market correction to have only modest negative macroeconomic effects

Monday, July 13, 2015 10:54 AM UTC

Editor's Picks

- Market Data

Most Popular