Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  Goldman AM Sees Strong Buyout Opportunities in Japan, South Korea and Australia

Goldman AM Sees Strong Buyout Opportunities in Japan, South Korea and Australia  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook

Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook  Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher

Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone

Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone  Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

- Latest data suggest that the slowdown in China is real. Last year GDP has slowed to multi decade low to 7.4 percent. This year it is widely expected that government will reduce the GDP estimate further towards 7%.

- Even the GDP fell in China or falls further towards 7 percent, it is a commendable number compared to developed nation. Chinese economy grew to become the second largest in the world and after long double digit growth a period of cooling is natural and manageable.

- Peoples Bank of China (PBOC) has cut the benchmark interest rate twice to current 5.35 percent. It also in February reduced the reserve requirement by 50 basis points.

- Deeper look at situation suggests that these cuts were introduced not from growth concern but reduce the burden of corporate debt and keep ample liquidity in the system in events of failure.

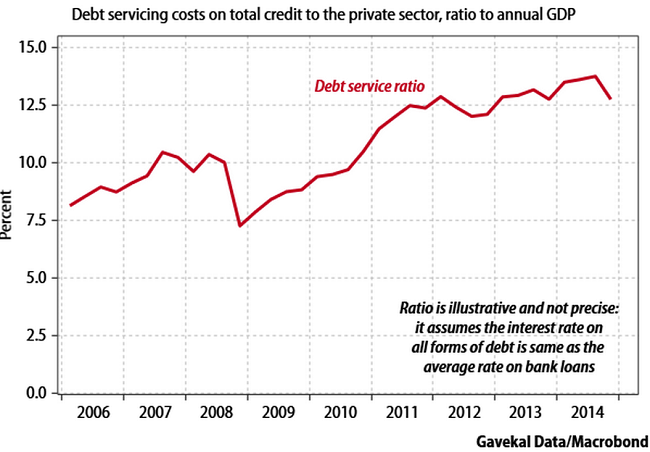

- Total debt in China could be as high as 240 percent of the GDP and non-government debt close to 200 percent of GDP. Even after the reduction debt service cost remains elevated above 10 percent.

- Chinese companies have been experiencing very high debt service costs well above 10 percent since 2010. Chinese companies have also gobbled up lots of dollar denominated debt which could become costlier to service in event of rates rise by Federal Reserve and fall in Yuan against dollar.

Swings in the Yuan rates and failure of the Chinese stock market to hold gains even after fall in interest rate suggest that market remain cautious over the situation. The Yuan could continue its fall against dollar in coming months. Yuan is currently trading at 6.274 down 0.3% for the day. CSI300 is trading at 3263 down 2.1% for the day.