Wall Street Ends Lower as AI Stocks Drag Markets, Fed Rate Outlook Shifts

Wall Street Ends Lower as AI Stocks Drag Markets, Fed Rate Outlook Shifts  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  US Dollar Slips After PCE Inflation Data as Fed Rate Hike Expectations Stay Elevated

US Dollar Slips After PCE Inflation Data as Fed Rate Hike Expectations Stay Elevated  Gold Prices Rise Above $4,000 as Inflation Data and Weaker Dollar Boost Demand

Gold Prices Rise Above $4,000 as Inflation Data and Weaker Dollar Boost Demand  Trump Urges Gasoline Retailers to Cut Prices to $2.50 Per Gallon, Warns of Legal Action

Trump Urges Gasoline Retailers to Cut Prices to $2.50 Per Gallon, Warns of Legal Action  Economic pessimism has set in – but there are reasons for Australians to be hopeful

Economic pessimism has set in – but there are reasons for Australians to be hopeful  S&P Affirms Brazil’s BB Credit Rating with Stable Outlook Amid Fiscal Challenges

S&P Affirms Brazil’s BB Credit Rating with Stable Outlook Amid Fiscal Challenges  US Stock Futures Rise as US-Iran Ceasefire Hopes Boost Market Sentiment

US Stock Futures Rise as US-Iran Ceasefire Hopes Boost Market Sentiment

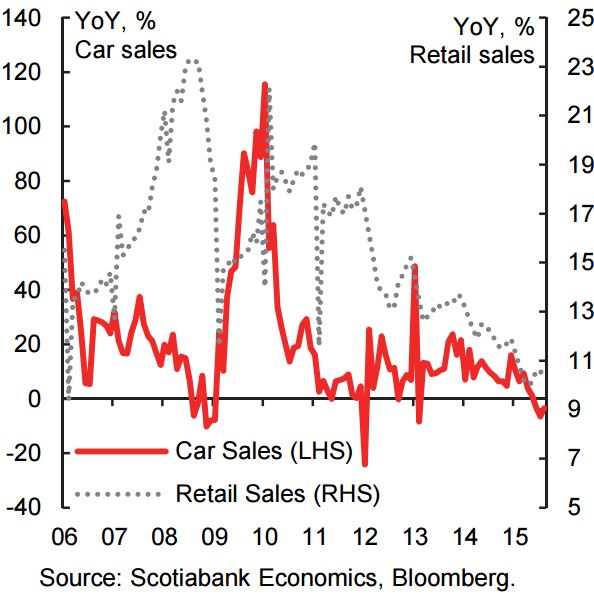

In an effort to revive the country's auto sector, China's State Council announced on September 30th that the sales tax on the purchase of vehicles with engine capacity of less than 1.6 liters (i.e. most passenger cars) would be halved, from 10% to 5%. This reduction took effect on October 1st, and will remain through to the end of 2016. The move may seem minor, but it has important economic and policy implications worth recognizing in the broader China context, according to Scotiabank.

China's auto industry has experienced rapid growth over the past decade, with sales volumes surpassing the United States in 2009 to become the world's largest auto market. Car purchases year-to-date remain on a record-setting pace and we forecast annual sales, including SUVs, will reach 19 million by the end of 2015. However, more recently, concerns about the sector have risen as the momentum behind purchases and output has moderated. Passenger car purchases y/y fell into negative territory in June of this year and were at -3.4% y/y in August. While it's true that most economic activity indicators have softened this year, car sales have been particularly weak in recent months, substantially underperforming overall retail sales growth of +10.8% y/y.

The tax cut may initially appear to be a narrow fiscal target, but our sense is that the move is intended to stimulate broader economic growth. It also highlights the importance of the auto industry to the Chinese economy. We estimate that auto sales and production account for more than 10% of the economy. More than 70% of all passenger vehicles sold in China have engine capacity of less than 1.6 liters, so the tax cut is well targeted to hit the majority of the sector. From a demand-side perspective, there is plenty of capacity for the industry to grow domestically: the G7 average car ownership rate currently runs at 689 per 1,000 people, while China currently has only 104 cars per 1,000 people. From a supply-side perspective, vehicle sales have increased at a double-digit pace over the past decade and automakers continue to add capacity in China, leading to the risk of significant excess capacity if sales stall for an extended period.

History also suggests that car sales will improve following a tax cut. In January of 2009, China similarly halved the sales tax on passenger cars from 10% to 5% to bolster a weak market. Sales immediately jumped 19% m/m, and vehicle sales turned from a negative year-over-year performance in the final months in 2008 to full-year growth of 53% in 2009. While the impact will likely be more subdued in this slower growth environment, we expect the tax cut to help support the purchase of at least an additional one million vehicles.

From a policy perspective, the tax cut is significant for three reasons. First, the move emphasizes policymakers' ongoing focus on the auto sector as a key driver of growth and employment. Last month, the PBOC cut the required reserves ratio (RRR) for auto-financing firms by 350 bps, much more than the 50bps cut for banks. Second, the tax cut is an example of policymakers relying more directly on fiscal stimulus to bolster growth, consistent with their goals of deleveraging. Moreover, the expiry date on the stimulus, valid only until December 2016, is clearly intended to create an immediate jumpstart to growth. Third, the move signals increased emphasis on the consumer as the next driver of growth, targeting underlying demand as opposed to, for example, cutting the RRR for financing firms, a supply-side maneuver.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

China’s auto sales tax cut is a key economic and policy move worth monitoring

Sunday, October 11, 2015 11:23 AM UTC

Editor's Picks

- Market Data

Most Popular