Ethereum Retreats Toward USD 2,000: Technicals Signal Caution as ETH Mimics Bitcoin’s Pullback

Ethereum Retreats Toward USD 2,000: Technicals Signal Caution as ETH Mimics Bitcoin’s Pullback  FxWirePro: EUR/ NZD steadies around 2.0150, retains bid tone

FxWirePro: EUR/ NZD steadies around 2.0150, retains bid tone  NZDJPY Bears Take Control: New Zealand Dollar Retreats as 92 Resistance Holds Firm

NZDJPY Bears Take Control: New Zealand Dollar Retreats as 92 Resistance Holds Firm  FxWirePro: EUR/AUD eases slightly but trend is still bullish

FxWirePro: EUR/AUD eases slightly but trend is still bullish  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro: GBP/USD recovers but bears are not done yet again

FxWirePro: GBP/USD recovers but bears are not done yet again  FxWirePro- Woodies Pivot(Major)

FxWirePro- Woodies Pivot(Major)  Bitcoin Battles Volatility: Institutional Support Eyes USD 64,000 Floor Amid Geopolitical Tensions

Bitcoin Battles Volatility: Institutional Support Eyes USD 64,000 Floor Amid Geopolitical Tensions  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  Pound Under Pressure as Yen Stabilizes: GBPJPY Bears Target 208 as Key EMAs Hold Resistance

Pound Under Pressure as Yen Stabilizes: GBPJPY Bears Target 208 as Key EMAs Hold Resistance  FxWirePro: USD/CNY gains some ground but bearish outlook persists

FxWirePro: USD/CNY gains some ground but bearish outlook persists  FxWirePro: GBP/USD outlook weaker on renewed downside pressure

FxWirePro: GBP/USD outlook weaker on renewed downside pressure  FxWirePro: USD/ZAR fibo rejection triggers sizeable pullback

FxWirePro: USD/ZAR fibo rejection triggers sizeable pullback  FxWirePro- Major European Indices

FxWirePro- Major European Indices  FxWirePro: GBP/NZD remains buoyant, looks to extend gains

FxWirePro: GBP/NZD remains buoyant, looks to extend gains

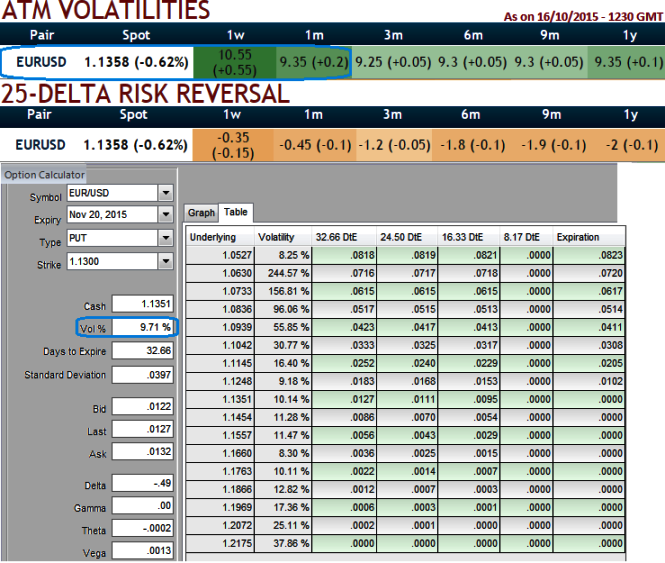

It is quite common market practice to recapitulate the information in sequence of the vanilla options market in the volatility smile table which includes Black-Scholes implied volatilities for different maturities and moneyness levels.

The degree of moneyness of an option can be corresponded to the strike or any linear or non-linear transformation of the strike. (Forward-moneyness, spot-moneyness, delta).

The implied volatility as a function of moneyness for a fixed time to maturity is generally referred to as the smile. The volatility smile is the crucial object in pricing and risk management procedures since it is used to price vanilla, as well as exotic option books.

For an instance, EURUSD ATM vanilla option has IV at 10.55% for 1w maturities, 9.35% for 1m maturity, but on a strategy or of different strike it certainly varies. When we've chosen a slightly out of the money strike put considering delta risk reversal computations the volatility has also been inched up at 9.71%. This is basically because market participants order flows do not expect the direction the strike price that is chosen.

That is because the market participants entering the FX OTC derivative market (heterogeneous) are confronted with the fact that the volatility smile is usually not directly observable in the market. This is in opposite to the equity market, where strike-price or strike-volatility pairs can be observed.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

A glimpse on why does volatility smile vary from different strikes and asset classes

Monday, October 19, 2015 9:42 AM UTC

Editor's Picks

- Market Data

Most Popular