FxWirePro: USD/CNY slips as strong China exports data Lift yuan

FxWirePro: USD/CNY slips as strong China exports data Lift yuan  FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data

FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro: AUD/USD eases as investors switch focus to RBA

FxWirePro: AUD/USD eases as investors switch focus to RBA  AUDJPY Bears Poised: Sell Rallies at 111.55 for 108 Target with 112.20 Stop

AUDJPY Bears Poised: Sell Rallies at 111.55 for 108 Target with 112.20 Stop  FxWirePro : USD/CAD falls as strong Canadian jobs data lifts loonie

FxWirePro : USD/CAD falls as strong Canadian jobs data lifts loonie  FxWirePro: NZD/USD retreats as Middle East instability weighs

FxWirePro: NZD/USD retreats as Middle East instability weighs  Major Pair Currency Score: NZD/USD and AUD/USD Lead Forex Rally with Perfect 100 Scores

Major Pair Currency Score: NZD/USD and AUD/USD Lead Forex Rally with Perfect 100 Scores  DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80

DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80  NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop

NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop  FxWirePro: EUR/ AUD neutral in the near term, scope further downside

FxWirePro: EUR/ AUD neutral in the near term, scope further downside  FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data

FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data  EUR/USD Rockets Past 1.1560 as Soft U.S. Jobs Data Fuel Fed Rate-Cut Surge

EUR/USD Rockets Past 1.1560 as Soft U.S. Jobs Data Fuel Fed Rate-Cut Surge  FxWirePro: GBP/AUD eases slightly, focus on near-term support

FxWirePro: GBP/AUD eases slightly, focus on near-term support

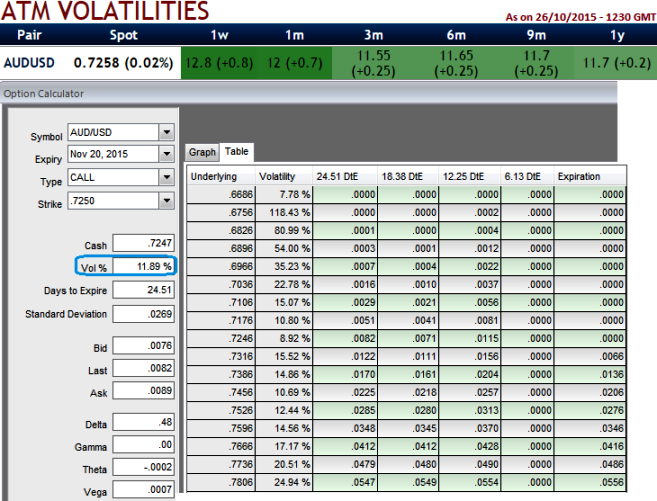

Firstly, let's have a glance on IV nutshell of AUDUSD, it is quite regular market practice to recapitulate the information in sequence of the vanilla options with no hedge scenario in the volatility smile table which includes Black-Scholes implied volatilities for different maturities and moneyness levels.

The degree of moneyness of an option can be corresponded to the strike or any linear or non-linear transformation of the strike. (Forward-moneyness, spot-moneyness, delta).

The implied volatility as a function of moneyness for a fixed time to maturity is generally referred to as the smile.

The volatility smile is the crucial object in pricing and risk management procedures since it is used to price vanilla, as well as exotic option books.

For an instance, AUDUSD ATM vanilla option has IV at almost close to 13% for 1w-1y maturities, but has been plummeting gradually to 12% over the period, also on a strategy or of different strike it certainly varies.

When we've chosen a slightly out of the money strike put considering delta risk reversal computations the volatility has also been inched up at 9.71%.

This is basically because market participants order flows do not expect the direction the strike price that is chosen.

That is because the market participants entering the FX OTC derivative market (heterogeneous) are confronted with the fact that the volatility smile is usually not directly observable in the market.

This is in opposite to the equity market, where strike-price or strike-volatility pairs can be observed.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Volatility smile varies with strikes – a glimpse on AUD/USD volatility skew

Tuesday, October 27, 2015 12:29 PM UTC

Editor's Picks

- Market Data

Most Popular