FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Asian Stocks Slip as AI Rally Fades, Oil Holds Steady on Iran Peace Deal Hopes

Asian Stocks Slip as AI Rally Fades, Oil Holds Steady on Iran Peace Deal Hopes  Asian Stocks Slide as Semiconductor Selloff Weighs on South Korea and Japan

Asian Stocks Slide as Semiconductor Selloff Weighs on South Korea and Japan  Gold Prices Surge 7% as Dollar Falls, Fed Rate Hike Bets Ease

Gold Prices Surge 7% as Dollar Falls, Fed Rate Hike Bets Ease  Gold Prices Steady as Hormuz Tensions Fuel Fed Rate Concerns

Gold Prices Steady as Hormuz Tensions Fuel Fed Rate Concerns  China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade

China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade  China Trade Surplus Beats Forecasts in July as Exports Stay Strong

China Trade Surplus Beats Forecasts in July as Exports Stay Strong  Wall Street Ends Mixed as Dow Hits Record Despite Tech Weakness

Wall Street Ends Mixed as Dow Hits Record Despite Tech Weakness  US Stock Futures Rise as Markets Await July Payrolls Data

US Stock Futures Rise as Markets Await July Payrolls Data

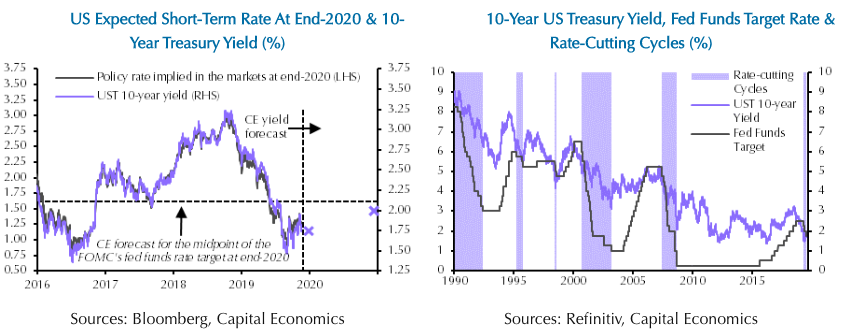

US Treasury yields have rebounded over the past few weeks, as worries about the US-China trade war and the outlook for the global economy have eased somewhat. But while they are not expected to revisit their lows, Treasury yields are also unlikely to rise much further over the next couple of years, according to the latest research report from Capital Economics.

Since falling within touching distance of its all-time low in early September, the 10-year Treasury yield has risen by about 30bp, to 1.75 percent. This rebound reflects mainly rising optimism about the US-China trade negotiations, which has led investors to pare back their expectations for further Fed policy loosening.

In addition, the improvement in risk sentiment has reduced demand for safe havens – gold and the yen have fallen by 5 percent and 2 percent, respectively, over the same period. Investors’ fears about deflationary risks also appear to have eased a bit – the inflation compensation implied by 10-year TIPS has risen by about 10bp.

Bond yields had fallen too far in September, because the economy was seen as slowing rather than falling off a cliff and that the Fed would not deliver as much easing as investors anticipated (at the time, the fed futures market implied an expected short-term rate of 0.75-1 percent by the end of 2020.)

Today, the market has largely come around to that view; investors do not expect further easing from the Fed in the next few months and discount only one more 25bp cut by the end of next year, which would take the Fed’s target band to 1.25-1.5 percent, the report added.

While the Fed is more likely to keep interest rates on hold, there is no longer a major difference between Capital Economics’ forecast and investors’ expectations. The report forecasts that the Fed policy is consistent with the 10-year yield rising only slightly in 2020.

The 10-year Treasury yield has tended to bottom out around the end of the Fed’s easing cycle. This suggests that, if we are right that the Fed will remain on hold from here, it is unlikely that the Treasury yield will revisit its September low, unless there is another severe bout of risk aversion or a major shift in policy.

"At the same time, although we think that the US economy will turn the corner in the first half of 2020, we also don’t expect it to rebound strongly thereafter. Instead, we anticipate mediocre growth and subdued inflation over the next few years, in both the US and the rest of the global economy. In that environment, it is unlikely that the Fed will start tightening policy anytime soon," Capital Economics further commented in the report.

Meanwhile, the upshot is that the 10-year Treasury yield is not expected to rise much further, and we now forecast it to stay around 2 percent for the next couple of years. While that is low by historical standards, it is in line with the downward trend over the past three decades, during which both inflation and real economic growth, and therefore the ‘neutral’ interest rate required to keep the economy in balance, have fallen.