Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing

Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing  BOJ Rate Decision in Focus as Yen, Inflation, and Nikkei Hang in Balance

BOJ Rate Decision in Focus as Yen, Inflation, and Nikkei Hang in Balance  Rubio Discusses Iran Crisis and Strait of Hormuz Disruptions With UK and Australia

Rubio Discusses Iran Crisis and Strait of Hormuz Disruptions With UK and Australia  Kevin Warsh Advances Toward Fed Chair Role Amid Political Tensions

Kevin Warsh Advances Toward Fed Chair Role Amid Political Tensions  Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns

Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  South Korea Central Bank Signals Inflation Concerns as Oil Prices Surge

South Korea Central Bank Signals Inflation Concerns as Oil Prices Surge

As inflation expectations rise globally, the US Federal Reserve is expected to hike rates at a faster pace next year. Last week, FOMC forecasted 3 rate hikes, compared to just one each in previous two years. Then why the governments are still able to sell bonds at negative rates? Last Friday, the United Kingdom for the first time sold bonds at negative rates. The government was able to borrow £1 billion at minus 0.1038 percent. The negative bond universe is squeezed but still close to $10.8 trillion. In August, this universe was as big as $13 trillion.

Part of the answer lies with Quantitative Easing. Several major central banks around the world are still pursuing quantitative easing. The European Central Bank (ECB) earlier this month announced a further purchase of €540 billion bonds till December 2017, once the current program expires in March 2017. Not only that, the ECB announced that it would now purchase below the deposit rate, which is at -0.4 percent. Since the ECB announcement, German 2-year yield has been declining to record low and currently trading at -0.8 percent.

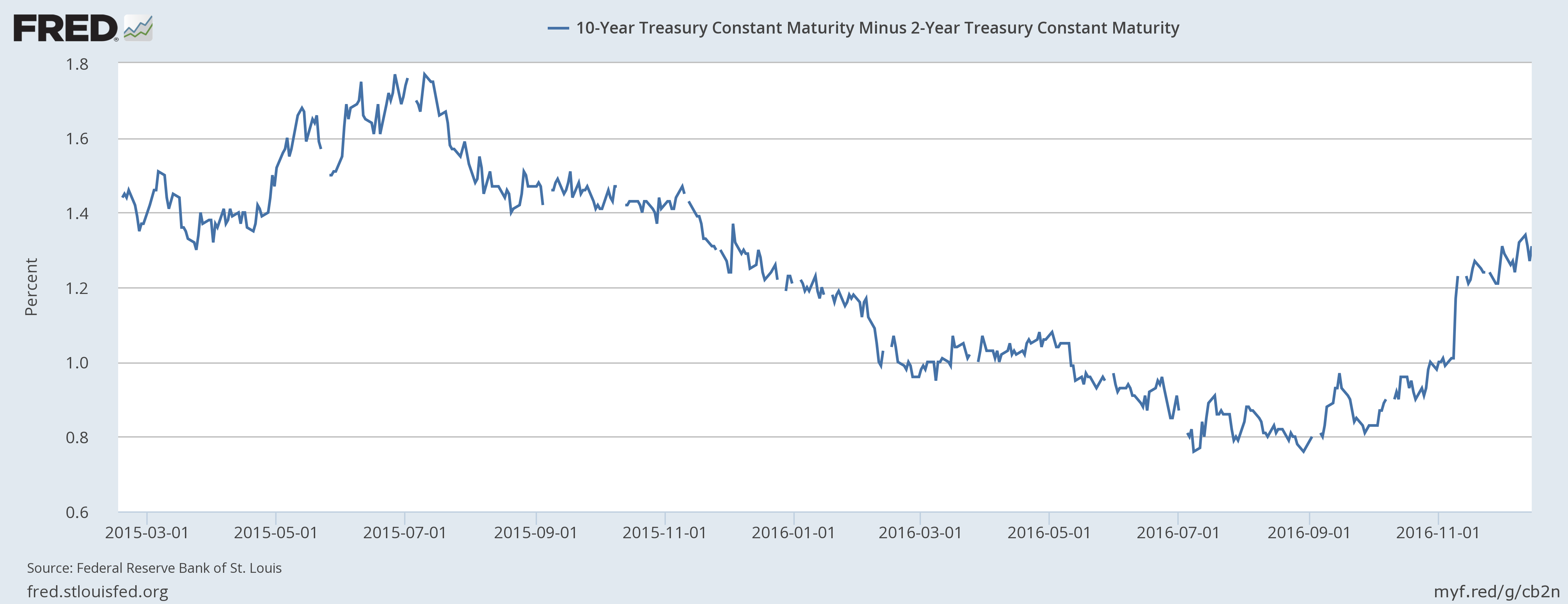

With rising inflation expectation globally, the market is and will return to the very fundamental that the central banks can control the short term rates but have hardly any control over the longer end of the curve, which gets determined by a variety of factors in the economy. The spread between the US 2-year and 10-year treasury has jumped by 56 basis points since September to 1.32 percent.