Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts

Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts  BOJ Governor Kazuo Ueda Hints at Rate Hike as Inflation Pressures Build

BOJ Governor Kazuo Ueda Hints at Rate Hike as Inflation Pressures Build  BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns

BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns  South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions

South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions

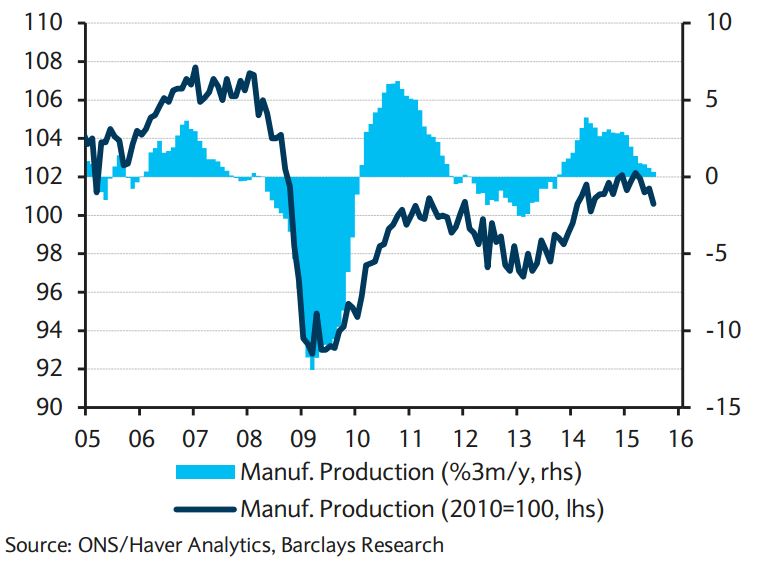

UK industrial production fell for the second consecutive month (-0.4% m/m, 0.8% y/y in July after -0.4% m/m, 1.5% y/y in June), while manufacturing registered a significant downward surprise (-0.8% m/m, -0.5% y/y in July after 0.2% m/m, 0.5% y/y in July). This weaker-than-expected print was echoed by the EEF Q3 Outlook Report in which the EEF, the manufacturing representative body, more than halved its manufacturing growth forecast; at the start of the year it was at 1.7% for 2015 whereas now it is at 0.7%. Of particular concern is the significant drop in investment goods, which has begun to show trend weakness, and the potential spill over this would have on economic activity if weakness continues. The carry over for production in Q3 is now at -0.6% q/q, its weakest since Q4 12.

International trade also showed substantial downside in July, with exports falling 9.5% m/m in real terms, cancelling out a strong second quarter; particular declines were noted in consumer goods and passenger cars. Geographically, weakness came from exports to non-EU countries, falling 15.1% m/m, while EU exports contracted by only 3.7% m/m.

The BoE kept its policy stance broadly unchanged and the balance of voting remained at 8 against 1 in favour of the status quo. The minutes of the meeting were fairly balanced, according to Barclays, with the MPC highlighting that it was still too early to draw conclusions from the latest developments in China and their possible impact on the UK economy. That said, the reference to a "finely balanced decision" for some members has been dropped, highlighting that at the margin, the Bank shifted to a slightly more dovish stance.

The discussion relating to the impact of recent market turmoil and Chinese growth transition confirmed initial thoughts that it would not change the BoE's policy rate strategy, for now. The committee nonetheless acknowledged that it was monitoring the situation closely. In contrast, the domestic outlook was a reason to cheer for the MPC. For Ian McCafferty, this was actually reason enough to vote for a rate hike again. The Bank builds its optimism on the latest Q2 GDP release, the strengthening outlook for household income and the still high levels of confidence, albeit the BoE downgraded its Q3 growth forecast from 0.7% q/q to 0.6% q/q. Even if the most recent data and surveys came in on the soft side, the Bank believes that the message from the August Inflation Report still holds and that levels of activity will remain elevated despite headwinds from the global economy and fiscal consolidation.

"We believe that Minutes were overall fairly balanced but at the margin, the language was more dovish, in particular with the removal of the reference that for some members the decision was finely balanced. While this view could be restored quickly, if the situation and the data were to surprise on the upside, it has to be assessed against the background of other central banks also becoming more cautious. Hence, it make sense for the MPC to become slightly more dovish, if only to limit the upwards pressure on the currency," commented Barclays.