Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  Asian Stocks Cautious Ahead of US Jobs Data as Oil Rises

Asian Stocks Cautious Ahead of US Jobs Data as Oil Rises  Singapore Says One-Third of U.S. Exports Hit by New 12.5% Tariff

Singapore Says One-Third of U.S. Exports Hit by New 12.5% Tariff  Gold Price Hits Seven-Week High as Fed Rate Hike Bets Fade and Hormuz Deal Hopes Grow

Gold Price Hits Seven-Week High as Fed Rate Hike Bets Fade and Hormuz Deal Hopes Grow  Oil Prices Slip as Hormuz Shipping Progress and Rising U.S. Crude Stocks Weigh on Market

Oil Prices Slip as Hormuz Shipping Progress and Rising U.S. Crude Stocks Weigh on Market  US Dollar Falls as Weak July Jobs Report Dents Fed Rate Hike Bets

US Dollar Falls as Weak July Jobs Report Dents Fed Rate Hike Bets  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise

US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise  US Stock Futures Hold Steady as Iran Hormuz Deal and Earnings Shape Market Sentiment

US Stock Futures Hold Steady as Iran Hormuz Deal and Earnings Shape Market Sentiment  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade

China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade

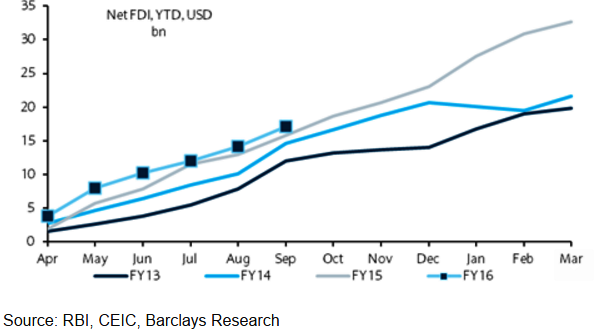

Inorder to increase inflows to India , the government has taken many steps in a major liberalisation of FDI regime. 15 sector's FDI regulations have been eased, limit on Foreign Investment Promotion Board(FIPB) is extended to INR50bn from INR30bn. These changes will lead to quicker FDI approvals, also by reducing paperwork.

Rules on FDI have also been diluted in wholesale and retail activities, defence sector, private banks and construction sector, helping improve job creation, boosting the sectors.

Capital account signals will be further opened up, which indicates government's willingness to undertake reforms, besides political setbacks recently.

Government has been easing FDI regime since it took powers, USD17.1bn of net inflows are seen in first half of 2015, last year net FDI was USD 32 bn, following a series of liberalisation steps since September 2015, when Government in conjuction with Reserve Bank, announced opening of bond market to greater foreign paarticipation.

Indian government also started a bankruptcy draft code, with further fiscalisation of oil price profits by indirect taxes.

"The challenge remains in getting parliamentary approvals for key tax reforms such as the Goods & service tax, which requires two-thirds majority approval from both houses of parliament", says Barclays in a research note.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Indian government takes major FDI liberalization moves, key reform approvals remains a challenge

Wednesday, November 11, 2015 5:37 AM UTC

Editor's Picks

- Market Data

Most Popular