Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why

Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why  Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert

Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy

Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data

Within next fortnight or so, we have series of monetary policy meetings lined up. A very low supply of economic surprises currently is by itself enough to explain the low level of market volatility.

RBA’s cash rate today is unchanged at 1.50%

ECB’s minimum bid rate on June 8th.

Federal Reserve of US on June 14th.

SNB’s LIBOR rate on June 15th.

BoE’s monetary policy summary and bank rates on June 15th.

BoJ’s monetary policy rate on June 16th.

Market volatility, both realized and implied, has declined across all asset classes this year, returning to the historical low seen during the middle of 2014. Despite its currently low level, market volatility is thus far from unprecedented

We proxy economic surprises by the standard deviation of weekly changes in J.P. Morgan's Forecast Revision Index (FRI) for global real GDP growth.

The current level of 3-month implied volatility across five asset classes is very much in line with our economic surprise proxy.

Leverage also matters for market volatility. We tend to think of market volatility as the product of the supply of surprises (news) and the vulnerability of markets to these surprises (leverage).

In terms of leverage, potential vulnerabilities lie with individual equity investors in the US, the leverage of which rose back to the historical highs seen in the middle of 2015, and non-financial corporates in China, the leverage of which remains stubbornly high.

The retrenchment of active managers, who are being crowded out by central bank QE in the bond space and a shift towards ETFs in the equity space, acts as the long-term depressant of market volatility.

Equally important as a long-term depressant of market volatility is a persistently high amount of excess cash balances by non-bank investors globally, which in our opinion backstops both equities and bonds and reduces downside volatility.

What is causing the decline in volatility? In our previous work “Volatility, Leverage and Returns”, it has been thought of market volatility as the product of the supply of surprises (news) and the vulnerability of markets to these surprises (leverage).

For example, an unexpected central bank policy change (the “surprise”) can change bond and equity prices by raising the expected path for growth and/or inflation. The actual price move and, thus, volatility are driven by the degree to which this policy news affects inflation and growth expectations, as well as uncertainty (i.e. the vulnerability or sensitivity of asset prices to the surprise).

This sensitivity should be driven by the degree to which the surprises induce investors to change their positions, which in turn would be driven by their leverage, by their risk capital and by the cost of trading.

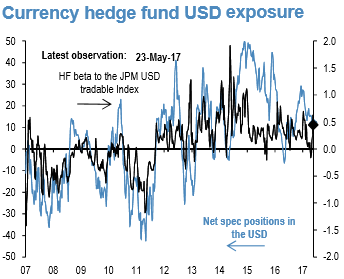

FX hedge fund USD exposure (refer above chart): The rolling 21-day beta of the Barclay Hedge FX index with the JPM USD tradable index vs. the net spec position in the USD as reported by the CFTC. Spec is the non-commercial category from the CFTC. Net spec position below is with one week’s lag.