U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand

JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate

Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate

Last Friday, the front end of the Canadian rates market priced a 30% chance that rates would go up this year. One speech from BOC Senior Deputy-Governor Carolyn Wilkins later, and pricing is over 50%. She cited broadening growth across sectors, a reduced drag from soft oil prices and solid Q1 growth as reasons for optimism.

What is striking isn’t so much the tone however as the market reaction. That reflects underlying CAD bearish views and positioning and a sensitivity therefore to any upbeat news or signs of hawkishness. We think CAD is the cheapest of the four G10 dollars, and it’s that valuation that gives it room to rally further over time (albeit probably after a pause now).

The wider significance of the BOC move is that the reaction to anything hawkish from central bankers outside the US will trigger a bigger reaction than anything they say that is dovish at the moment.

We could foresee a bullish scenario of USDCAD above 1.43 driven by:

1) The US moves ahead on border adjustments or NAFTA negotiations turn sour;

2) US-Canada trade negotiations turn acute and negative with a proliferation of high-profile trade enforcement actions by the US;

3) Commodity prices fall much further on China/global growth concerns;

4) Wobbles in the housing market cause a broader instability in the financial system.

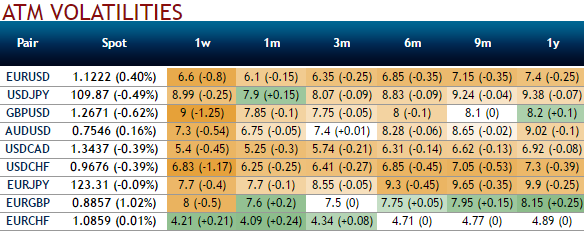

Please be noted that the above nutshell showing IVs and risk reversals of this pair, that has been neutral. Implied volatilities have been extremely lower (least among the G7 FX space) and you could also make out that there has been no hedging sentiments (neutral risk reversals in 1w tenors and with bullish neutral hedging sentiments in 1m-1y tenors).

Well, contemplating these OTC indications, using this option strategy, the investor gets to earn a premium on writing overpriced calls while at the same time appreciate all benefits of underlying spot outrights moderately. If he’s having FX payables unless he is assigned an exercise notice on the written call and is obligated to sell his spot outright holdings, this strategy is a risky venture.

This is a suitable strategy where the moderately bullish investor sells out of the money calls against a holding of the underlying spot outrights. The OTM covered call is a popular strategy as the investor gets to collect premium while being able to enjoy capital gains (albeit limited) if the underlying spot FX rallies.