2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Part II — The listing: NFTs as bottle-stamps, and a vault the family is in no rush to sell

Part II — The listing: NFTs as bottle-stamps, and a vault the family is in no rush to sell  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.

A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?

In this write-up, we run you through the DBS bank’s perceptive views on rate yields outlook in one emerging market in comparison with USTs.

The Central Bank of Malaysia maintained the status quo in its monetary policy, keeping benchmark interest rate unchanged at 3.25 percent on January 24th, 2019, as widely expected. Policymakers that the decision in consistent with the intended policy stance and they will continue to monitor the balance of risks surrounding the inflation and domestic growth outlook. The Committee also noted that the economy maintains its underlying fundamental strength, with steady economic growth, low unemployment, and a current account surplus.

Well, with growth outlook biased to the downside and inflationary pressures likely to stay benign, we expect Bank Negara Malaysia (BNM) to keep policy rates unchanged today (decision expected today at 3pm) and rest of the year. IRS markets are largely in line though pricing has recently moved from small chance of 1 hike to small chance of 1 cut.

Based on several valuation metrics, Malaysian Government Securities (MGS) look cheap. Real yields on 10Y bonds are elevated at 4.0% vs the long-term range of 1.0 - 2.5%. 10Y spread over US Treasury has surged to 130bps, high compared to other similarly-rated sovereign credits such as Poland (11bps) and Thailand (-30bps).

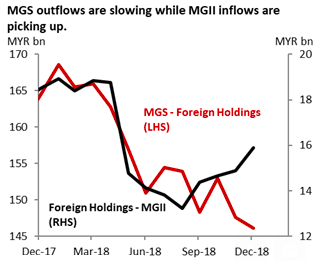

We recognize that some of the cheapness should be attributed to weaker fundamentals. Malaysia's fiscal position has worsened post-elections and reforms could take some years to complete. However, in our view, the government’s reform plans are credible and the risk of rating downgrades remains low (Moody’s recently reaffirmed Malaysia’s rating at "A3" and kept outlook "stable"). Looking at technicals, the pace of outflows from MGSs is slowing and Malaysia Government Investment Issues (MGII) are seeing healthy inflows lately. Positioning is probably light after 2018’s outflows and we could see some yield compression when inflows return. All considered MGSs are cheap even after accounting for the weaker fundamentals.

On a currency-hedged basis, MGS yields have turned very attractive. MGS-UST yield differentials have widened and the cost of hedging has declined. Courtesy: DBS & Bloomberg

Currency Strength Index: FxWirePro's hourly USD spot index is inching towards -73 levels (which is bearish) while articulating (at 10:30 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex