U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

The market is currently seeing the likelihood of three Fed rate hikes until late 2017 as standing at 50% – the highest level since the FOMC meeting in March. At the time the market was still convinced that there would be a further two rate steps until end-2016. Now we know that there will be only one more this year. The same 2017 likelihood as in March, therefore, has a completely new quality.

It signals market expectations of a much faster Fed rate hike cycle. Hardly surprising as the 5Y×5Y inflation expectations (i.e. the market bet on average US inflation rates for the period of 2021/26) has reached new highs.

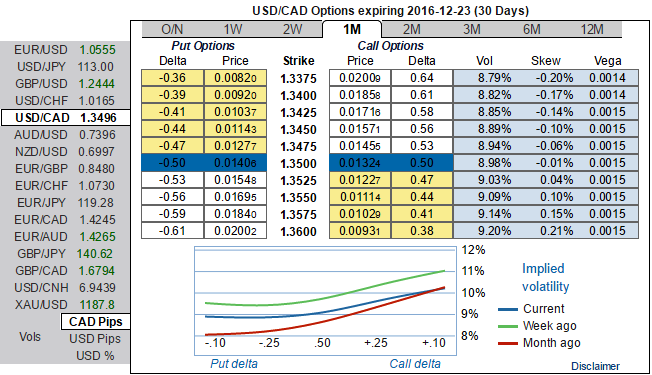

The FX Markets began pricing in owing to a Trump’s victory after the Republican candidate took the lead over the democrat. The U.S. dollar managed to bounce back vigorously after the US Election Day from the slumps of 1.3264 to the current 1.3496 levels during mid-European sessions.

The election of Donald Trump as the next US president saw the initial “risk-off” move properly trumped, as his acceptance speech was more conciliatory and the focus moved towards his fiscal policies. US equities, particularly the S&P500, flew back towards all-time highs, while the US yield curve steepened, led by 10-year yields racing up through 2%. This lent renewed support to the USD, especially versus G10.

On the flip side, the oil driven currency gaining upside traction ahead of OPEC’s meet that is scheduled on Nov 30th to coordinate a cut, potentially together with non-OPEC member Russia. OPEC may probably extend a proposition to other producers curtail their oil production by 880,000 barrels per day for six months starting from Jan. 1 2017, sources stated.

The implied volatilities of 1W USDCAD ATM contracts are trading 9.15%, while 1m IVs are just shy above 9%.

While these 1m IV skews are supportive of OTM call strikes, the premiums of 1W ATM contracts are trading at 14.75% more than NPV which is disparity between IVs and option pricing amid uptrend of the underlying spot FX, hence, comparing this disparity with bullish neutral risk reversals we think the opportunity lies in writing an OTM put while formulating below option strategy for USDCAD hedging.

Hedging Framework:

3-Way Options straddle versus OTM put

Spread ratio: (Long 1: Long 1: Short 1)

Rationale: Fed’s hiking speculation is the major booster for the dollar while crude price gains cushion CAD on the contrary, in this scenario eyeing on OTC price differentials to keep FX exposures optimally hedged.

How to execute:

Go long in USDCAD 1M at the money +0.51 delta call, go long 1M at the money -0.49 delta put and simultaneously, short 1w (1%) out of the money put with positive theta.