Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

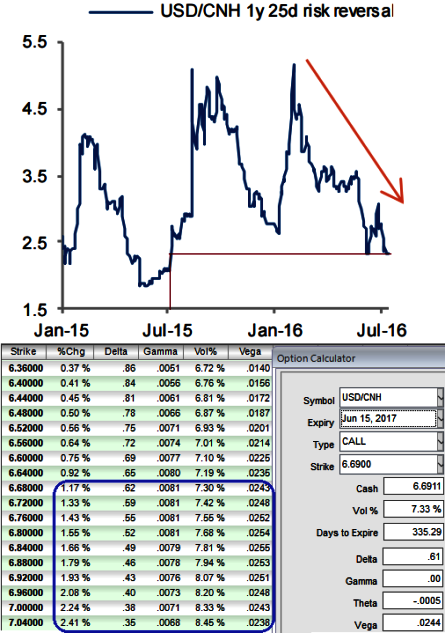

The Chinese economy grew 6.7% YoY in Q2 2016, unchanged from Q1, to bolster the growth in order to achieve 6.5-7.0% growth target, further monetary policy easing is still on the table. The slowdown in M2 growth in recent months hints that the PBoC has room to conduct monetary policy easing.

As stated in our recent write up on USDCNH IVs that shows the divergence with the realized volatility, shorting vega is advisable in such cases. Therefore, we call for below option strategy considering the on-going robust bullish environment last has lasted since 2014.

Buy USDCNH 1y Seagull strikes 6.55/6.85/7.20 Indicative offer: 0.42% (vs 0.82% for the call spread strikes 6.85/7.20, spot ref: 6.6910). This structure is a standard 1y call spread strikes 6.85/7.20 half financed by selling a put strike 6.55, offering beyond 7.20 a maximum leverage of 11x at the expiry.

With no digital risk involved and thanks to the limited convexity of long-dated options, the position can be conveniently delta-hedged if the spot moves lower in the early stages.

Risk reward profile: The 1y risk reversal is trading at a one-year low as shown in the diagram. It provides a good entry point to reload topside exposure despite the expensive volatility and also be noted that the healthy vega and gamma flashes on OTM call strikes. It also means that the vol market does not discount a disordered RMB depreciation, further supporting our short vega view.

Three-year-old depreciation trend reverses, the supply-demand imbalance in capital flows reaches equilibrium or hard-landing risks recede, causing the nearly three-year-old RMB depreciation cycle to reverse. The structure would face unlimited losses if USDCNH trades below the 6.55 strike in one year.

Vanilla calls or call spreads are too expensive when considering the probability-weighted terminal value of CNH a year from now. Under the premise that USDCNH only retraces a modest portion of the recent gains (similar to past experience when after an up move USDCNH did not revisit the lows and that there are no strong arguments for sustained appreciation on fundamental grounds, selling downside optionality can cheapen the cost of the call spread quite significantly.