Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields

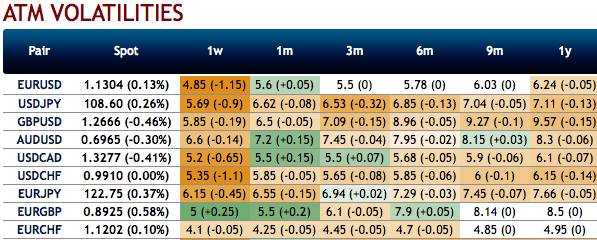

This has been a year of lower vols, especially among FX space. Just glance at the OTC FX markets, shrinking implied volatilities (IVs) are luring options writers. Please observe USDCHF and EURCHF are showing lower IVs despite the schedule of SNB’s monetary policy event for this week.

That is because the Swiss National Bank (SNB) has been maintaining the status quo in its monetary policy to leave everything unchanged (kept libor rate at -0.75%).

OTC Updates and Options Strategy:

Let’s just quickly glance through implied volatility (IV) nutshell before deep diving into the strategic frameworks of USDCHF. CHF crosses are showing the least IVs among G10 FX bloc (1m IVs are at 5.85 and 4.25 for USDCHF and EURCHF respectively). Hence, we advocate butterfly options spreads amid this lower vols environment.

The rationale: IV factor is highly imperative in FX option dynamics because the option pricing significantly depends on future volatility, and it is quite impossible for any veteran to ascertain accurate future volatility.

Nevertheless, it is quite possible to calculate the marketplace’s expected future volatility using the option’s price itself which is known as implied volatility (IV). Well, this is quite intuitive owing to the higher likelihood of the underlying spot FX market ‘swinging’ in your favor.

If IV increases and you are holding an option, this is good. On the contrary, if you have short on option, it is not desirable. The option writer likes IV to drop so the premium falls, thereby, the underlying price remains stagnant and he can pocket the initial premium received.

The execution of options trading strategy: Contemplating above rationale, the recommendation would be on buying OTM -0.49 delta put while simultaneously shorting ATM put with similar expiries and buy OTM 0.5 delta call while simultaneously shorting an ATM call with similar expiries. This strategy is structured for a larger probability of earning a smaller but certain profit as USDCHF is perceived to have low volatility.

The highest return for this strategy is achievable when the pair at expiration is equal to the strike price at which the call and put options are sold. At this price, all the options expire worthless and the options trader gets to keep the entire net credit received when entering the trade as profit.

Risk/Returns Profile: The maximum return occurs at ATM strike. A smaller return is made between ATM strikes and the break-even points. The maximum loss is limited by OTM strike prices.

Effect of Volatility: The value of the options will decrease as volatility decreases, which is usually conducive for the strategy. An increase in volatility will be generally bad for the strategy as stated above.

Effect of Time decay: The value of the option decays as each day passes (good).

Margin requirement: Depends on how it is constructed. Courtesy: JPM & Saxo

Currency Strength Index: FxWirePro's hourly USD spot index is inching towards 13 levels (which is mildly bullish), while hourly CHF spot index was at -18 (mildly bearish), while articulating (at 10:42 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex