Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings

Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges

Vega is usually expressed as the change in premium value per 1% change in implied volatility.

If the Vega of a long (buy) option position is USD 100 and IV increases or decreases by 1%, the option’s premium would also increase or decrease accordingly by USD100, respectively. The Vega of a short (sell) option position is negative and an increasing IV is bad.

Amid heightened sensitivity of macro markets to US inflation data and increasing discomfort about the twin US deficits, FX vols should remain supported. FX vol ownership at the belly of vol curve is particularly appealing.

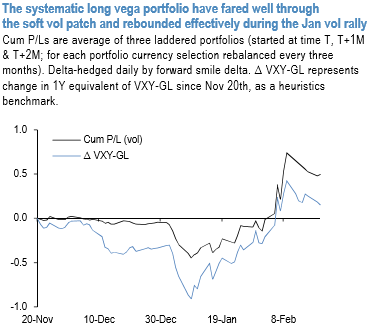

We back-tested a rule-based heuristics to owning long vega – i.e. systematically rotating long vega ownership across USD/G10 & EM based on a composite trading signal -constructed from three signals: 1-year z-score of CTP (carry to-premium ratio), strength of spot trend and 1-year z-score of realized/ATM vol ratio (for details: FX Volatility: Goldilocks is in the price, Nov 2017.

The rule-based trading made long vega worth sustaining 3-5vol pts of theta-decay annually, on average, in calm markets. The above chart shows the recent (out-of-sample) performance of the strategy. The systematic portfolio (three 1Y tenor straddles selected monthly and held for three months in laddered portfolios started at time T, T+1M & T+2M) have fared well through the December soft vol patch and rebounded effectively during the January vol rally. In the current market, the three vega longs that stand out based on the composite systematic signal are NZD, CHF and SGD vols.

FxWirePro launches Absolute Return Managed Program. For more details, visit: