ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve

ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated

Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing

Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing  Goldman Sachs Delays Fed Rate Cut Forecast to 2026 Amid Rising Inflation Concerns

Goldman Sachs Delays Fed Rate Cut Forecast to 2026 Amid Rising Inflation Concerns  BOJ Rate Hike Expectations Grow as Board Member Signals Hawkish Stance

BOJ Rate Hike Expectations Grow as Board Member Signals Hawkish Stance  DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects

DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

The US 10Y Treasury yield slipped from its four-year high of 3.03% to 2.98%, with most of the move occurring before the ECB decision. 2Y yields nudged higher, from 2.47% to 2.49%, to help flatten the curve. Fed fund futures yields continued to price the next rate hike in June as a 100% chance.

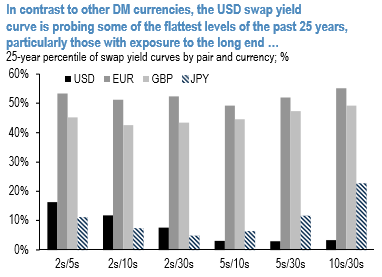

Despite new multi-year highs in Treasury yields for some sectors, focus in U.S. rates markets was squarely on the curve and going forward, the swap yield curve slope is increasingly exposed to more idiosyncratic factors via the term structure of swap spreads.

Though the recent re-pricing of the yield curve has not been particularly disorderly, its proximity to inversion has generated significant focus. This is certainly not unique to the U.S., but is more pronounced relative to other currencies (refer above chart). That is not to say flat curves are unprecedented, particularly if one adopts a global perspective. Starting with a simple historical comparison, the 2s/10s USD swap curve, for example, has been inverted for nearly 6% of the past 25 years while in GBP this was true nearly one-quarter of the time over the same period.

A key risk factor to our stance is the potential role of exotics hedging flows. Because certain types of payoffs — e.g., non-inversion and other range accrual notes — contain embedded binary optionality, rapid changes in the convexity profile of these exposures can lead to very disorderly rebalancing flows as dealers manage their exposure.

This has been an important consideration in the past for U.S. rates. That said, the stock of such exposures in USD notes is considerably smaller than was the case in 2006, reflecting a more narrow set of both investors and issuers, and the leverage of those exposures is much lesser as well.

These flows also only tend to arrive in force when the curve is meaningfully inverted, rather than right around zero.

Therefore, while potentially a driver of the swap yield curve for short periods of time, we expect neither a large nor a sustained impact on the swaps curve from exotics-related hedging. Courtesy: JPM

FxWirePro launches Absolute Return Managed Program. For more details, visit: