Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

As the U.S. Federal Reserve is most likely to maintain status quo at its monetary policy meeting today due to pauses to parse more economic data but may hint it is on track for an increase in June, bullion’s both spot and OTC markets have been highly active today.

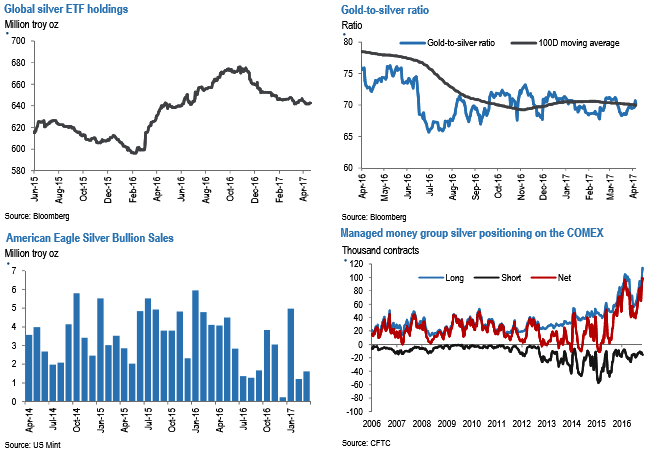

Turning to silver more specifically, following the mid-March Fed hike, silver prices outperformed gold into the end of the month, more than doubling the return of gold in the second half of March at around 8%. This sent the gold-to-silver ratio from about 71 down to below 68.5by the end of March (refer above diagram).

However, with silver largely ranging between $18/oz and $18.60/oz so far in April and gold moving another roughly $30/oz higher, the ratio has rebounded back up above 70.25 on silver underperformance.

In terms of investor flows, money managers have added more than 35,000 contracts of net length in COMEX silver over the past three weeks ending last Tuesday (April 11). This propelled their net long position to more than 98,800 contracts long, edging out last July to mark the longest level since data begin in 2006 (refer above diagram).

Particularly relative to investor positioning in gold which at around 140,000 contracts net long is roughly half the level it peaked out at in July 2016, silver length appears stretched. However, if last year is a guide, the silver net length did not exactly wash out lower after peaking in July 2016. Instead, it took about three months to bottom out at around 40,000 contracts net long.

Unlike the recent boost in investor length on the COMEX, total ETF holdings of silver have remained lackluster and range bound, roughly trending between 642 and 648 million ounces since the beginning of March (refer above diagram).

In terms of physical demand, higher prices likely led to lower sales of American Eagle silver coins so far this year. In the first quarter overall, sales declined by 47% yoy according to the US Mint, however, March sales were up 33% mom (refer above diagram). Furthermore, precious metals consultancy Metals Focus contends that while price likely played a role in subdued investor demand it might not be as weak as the US Mint’s numbers indicate.

Overall, investor demand on the COMEX has primarily driven silver prices higher so far in 2017 with ETF demand and physical investment appearing lethargic from the 1Q data we have. While questions still remain about how much additional physical demand will come from industrial sources this year, particularly photovoltaic installations after huge growth in 2016, we maintain our view expressed above that macro precious metals drivers like rates and FX will ultimately guide the price of silver in 2017.

To conclude, while silver prices could be maintained in the coming weeks on lingering risk-off sentiment around the French elections and other near-term catalysts, they will likely adjust lower into the second half of the quarter on higher US yields.