World game at war: why some European nations have threatened a World Cup boycott

World game at war: why some European nations have threatened a World Cup boycott  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  ‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online

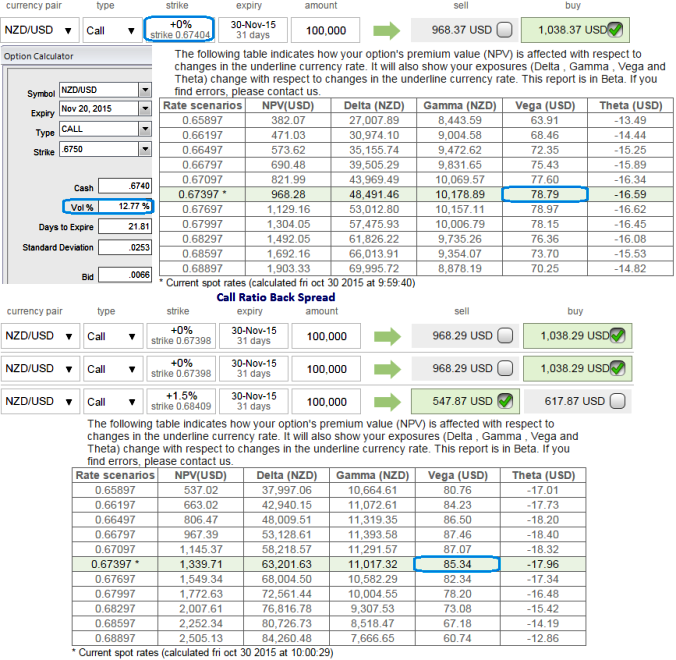

In between recovery rallies of Kiwi dollar we stated to use any dips for shorting in Call Ratio Backspreads in our previous posts (higher IV favored writers), it has shown their effects and is now heading again for attempts of recovery as both technical and fundamental indications are signaling buying sentiments.

The current IV of NZDUSD call is reducing to 12.77% from 14.59% which is good for option holders, usually if the Vega of a long option position is positive and the implied volatility rises or dips, the below stated option prices are directly proportional to the implied volatility.

Vega on Long ATM Call = 78.79 which has increased from earlier flashes when advised call back spreads.

So in this case Vega both on long position is reasonably acceptable.

Risky traders can still initiate shorts in this ITM call with positive theta but ensure shorter expiries on the same as it is desirable that at maturity the underlying exchange rate of NZDUSD to remain near short strikes in order to achieve highest returns.

Hence, we recommend it is better to cover all your shorts and as shown in the diagram purchase 1 ATM call and (1%) OTM call and simultaneously short 1 lots of ITM call with shorter expiry in the ratio of 2:1.

The lower strike short calls because it finances the purchase of the greater number of long calls (ATM calls are overpriced, so we chose 1% OTM calls as well) and the position is entered for no cost or a net credit.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Reducing vols with rising Vega good news for NZD/USD call holders – shorts in CRBS still an option for risky traders

Friday, October 30, 2015 5:15 AM UTC

Editor's Picks

- Market Data

Most Popular