Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts

Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts  Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns

Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns  RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200

RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200  BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns

BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns  Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing

Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing  South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions

South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions

On the macro side, with the chorus of hawkish commentary by the Fed officials, the market has priced in a March hike immediately. Given that, widening U.S.-Japan yield spreads have brought USDJPY higher and the pair is now reaching the upper end of its trading range since mid-January. We now expect the Fed to deliver three hikes in this year (Mar, Jun, and Sep vs. May and Sep previously).

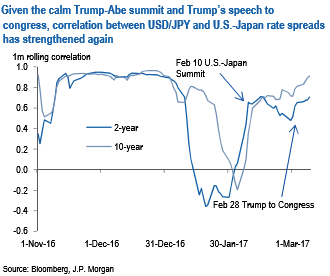

One important assumption of our bearishness on USDJPY is that a correlation between the pair and U.S.-Japan yield spread collapses with heightening concerns on political risks. Although it was the case early this year, the correlation has strengthened again as the U.S.-Japan summit and Trump’s speech to Congress passed without any troubles (refer above chart).

As a more harmonic U.S.-Japan relationship and a more aggressive Fed stance would mitigate downside risks to USDJPY to some extent, we revised USDJPY forecasts for end-June, end-September, and end-year to 111, 108 and 105 from 105, 102 and 99 respectively. We target 105 at end-March next year.

As the new profile suggests, however, we think factors mentioned above would not be influential enough to get USDJPY on a solid upward path heading to 120 or even higher, and still, expect it to track a modest downward trend in the medium-term.