Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data

Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data  US Yen Intervention Unlikely to Deliver Lasting Recovery, Yardeni Says

US Yen Intervention Unlikely to Deliver Lasting Recovery, Yardeni Says  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise

US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise  South Korean Won Leads Asian FX Losses as Dollar Rises

South Korean Won Leads Asian FX Losses as Dollar Rises  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  China Inflation Cools in July as CPI Misses Forecast, PPI Deflation Eases

China Inflation Cools in July as CPI Misses Forecast, PPI Deflation Eases  World game at war: why some European nations have threatened a World Cup boycott

World game at war: why some European nations have threatened a World Cup boycott  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue

Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue

The British economy advanced 0.6 pct on quarter in the three months to September of 2016, slowing from a 0.7 pct expansion in the previous period and in line with the preliminary estimate.

With no significant data announcements except UK PMIs that could drive volatility in both FX option as well as spot FX markets. 1w ATM IVs of GBPJPY are a tad below 13%, we think these vols are not justifiable despite a quite data flow in both UK and Japan.

Sterling slips to its weakest since mid-November amid an ongoing absence of clarity on UK’s EU exit plans. While GBPJPY has been struggling to break the stiff resistances of 144.662 levels amid recent rallies bullish SMA crossover, more rallies seem likely upon breach above 144.662 (we’ve explained the importance of this levels in our technical post), but any sharp spikes in near terms seem unlikely.

Bank of Japan keeps policy unchanged, retaining a 0% 10-year JGB yield target. Global PMIs for December eyed; UK survey momentum is expected to remain solid.

However, the PMI has provided a first taster. The coming week’s UK PMI data (Tue-Thu) and BoE credit data (Wed) will provide further color on Q4 trends. Survey data for December so far – including GfK consumer confidence and our own Business Barometer – have seen improvements relative to November, but sharp movements in surveys since the referendum have generally tended to have little carryover to official estimates of ‘hard’ activity.

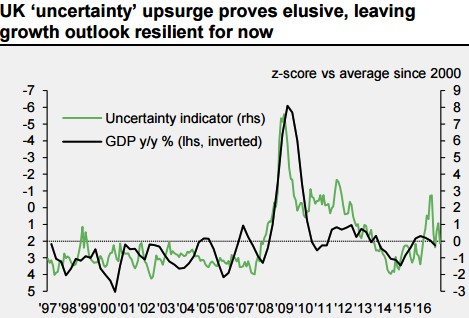

More broadly, with the post-referendum upsurge in uncertainty proving short-lived, the main drag on the economy is now expected to come through the hit to consumer purchasing power resulting from the weakness of sterling, with the bulk of the impact due to take effect in 2017.

In the recent times, GBP vols skews normalized too much after the Brexit votes, the GBP volatility market normalized sharply (you could observed that in GBPJPY IV skews) which is quite favorable for OTM option writers. The liquidity recovered and the extreme positioning was ultimately absorbed. The price action is not taking the direction of an imminent new trend. As a result, the option market aggressively unwound smile positions.

Major downtrend and short-term upswings into consideration, anyone who wishes to carry long GBPJPY exposures, a collar options trading strategy is recommended. This could be constructed by holding a total number of units of the underlying spot FX while simultaneously buying a protective put and shorting call option against that holding. The puts and the calls are both OTM options having the same expiration month and must be equal in a number of contracts.

The collar is a good strategy to use if the options trader is writing covered calls to earn premiums but wish to protect himself from an unexpected sharp drop in the price of the underlying security.