Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert

Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert

In global FX market, everywhere you see the only trendy voice that you could hear is that the US dollar weaker, weaker, weaker. USD only moves in one direction at the moment that is southwards. Be it against EUR, JPY or CNY: USD is easing on a broad basis. Against EUR it is slowly approaching the 1.20 mark. It is becoming gradually clear that the greenback is also suffering not only as a result of Fed’s recent guidance but also the President Trump’s weak government. It is unfair to give all credits on Fed’s kitty. Central banks’ policy divergence is the other predominant aspect to be considered.

The broad dollar ground lower in the recent times to make a fresh multi-month low even though the Fed indicated that balance sheet normalization is on the cards for September. The red flags for the currency came in on the back of a tweak in the Fed’s language on inflation was interpreted by markets as dovish and activity data beat expectations in Europe and Asia.

The US data released at the end of the week further reinforced bearish momentum for the dollar with the important quarterly employment cost index coming in below than expectations, thus indicating soft inflation pressures in the US.

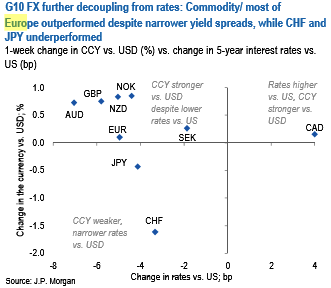

The macro theme of Europe leading outperformance remained dominant with Scandis outperforming in G10 on strong data/higher oil prices and EMEA in EM. Other remarkable market moves came from:

i) Swiss franc (EURCHF made a new high since the SNB abandoned the floor) on possible M&A flow and SNB comments that while not a departure from their previous stance, reiterated that their policy stance remains unchanged putting them in contrast with several other DM central banks where policy is evolving, and

ii) The commodity prices with oil and base metals higher across the board, giving commodity currencies a lift as well, despite narrower yield spreads (refer above chart). Against this backdrop, the portfolio has fared well in the past week.

In G10, longs in Europe (EUR, NOK) vs USD and JPY have broadly paid off while the performance of EM trades has been more mixed.

Recent FX market moves in G10 have been primarily about a divergence in central bank policy, so a strengthening in currencies where central bank policy is likely to or has already started to pivot (ECB, BoC) vs. those where central banks are likely to keep policy unchanged and stay dovish (BoJ and possibly SNB).BoC) vs those where central banks are likely to keep policy unchanged and stay dovish (BoJ and possibly SNB).