BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

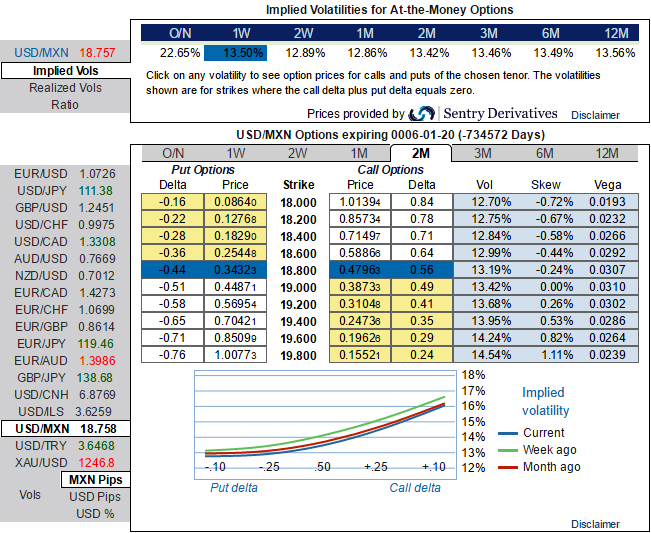

As regards the Bank of Mexico’s (Banxico) rate decision today analysts expect a further rate hike by at least 25bp. As this is largely priced in on the market the peso is unlikely to appreciate notably in the case of a 25bp rate hike. The central bank is under pressure to take action as inflation has risen notably over the past few months.

The central bank of Mexico raised its benchmark interest rate by 50 bps to 6.25 pct on February 9th, 2017, in line with market expectations. It was the fourth straight hike, bringing borrowing cost to the highest since April of 2009. The decision aims to protect the currency and to prevent additional inflationary pressures after the government increased gasoline prices.

Both the overall and the core rate had recently exceeded the central bank’s target rate of 3%. Important drivers are the depreciation of the peso until the end of January as a result of the US elections and also the Mexican government’s energy reform at the start of the year that led to a strong rise in petrol prices. At the same time, the peso is also an argument in favor of a small rate step.

The peso has regained most of the ground lost as a result of the Trump effect since the end of January. Against a currently peso friendly background 25bp should be sufficient today. The fact that some analysts are expecting a larger step is unlikely to lead to significant MXN losses.

Hedging Strategy:

After weekend’s correction in USDMXN from the highs of 18.75 levels, the pair is rejecting below resistance at 7DMA in the major uptrend and likely to show strength only at next strong support at 18.2890 (i.e.21EMA) to resume its previous bullish rallies, for now, the major uptrend appears to be robust and likely to prolong further. Hence, we use dips effectively to deploy shorts in OTM calls.

While ATM IVs of this pair is substantially spiking higher above 13.5% and 13.42% for 1w and 2m tenors and positively skewed IVs are signifying the hedgers’ interests in downside risks which is conducive for the holders of the call options, using the prevailing dips in this underlying pair writing narrowed tenor OTM calls would reduce the cost of hedging.

Thus, using any abrupt dips, initiate a diagonal debit/bull call spread (DDCS) at net debit.

The execution: Initiate shorts in 1W (1%) out the money calls with positive theta, simultaneously, buy 2M (1%) in the money 0.51 delta call option. Establish this option strategy if USDMXN spot FX is either foreseen to be in sideways or spike up considerably over the next month but certainly not beyond your upper strikes in short run.