Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says

AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch

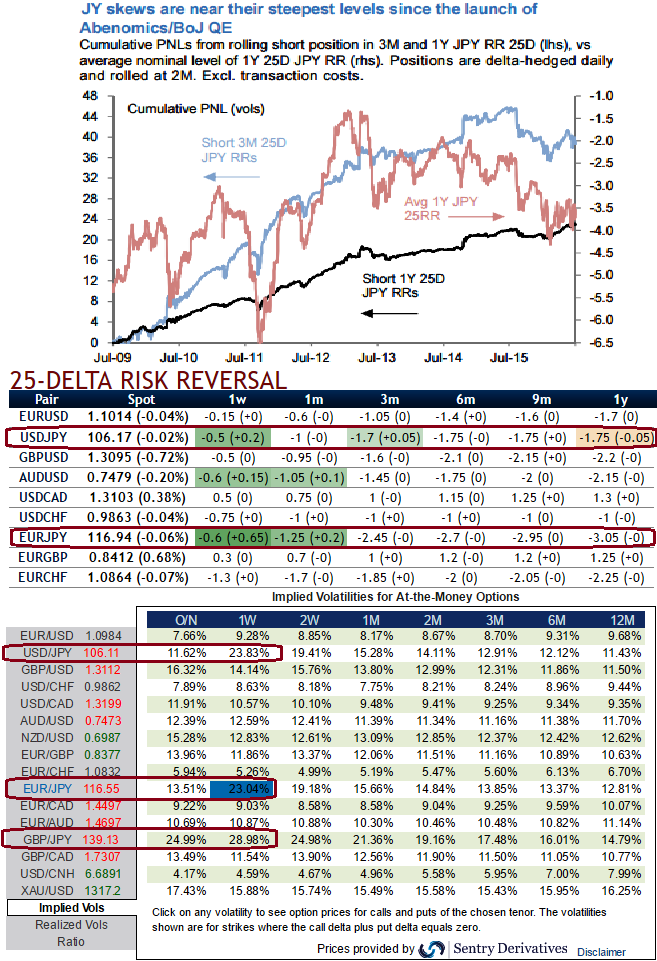

We hold short JPY skew risk as valuations are stretched. Short-dated tenors are exposed to BoJ under delivering this week, but longer dates offer consistently rich risk premia to fade.

JPY vol risk premia are extreme ahead of next week's BoJ meeting, with front end vols at their most elevated since Oct 2008. 1W expiries covering the BoJ are marked at a whopping 26.6, and the 1M-3M curve is at its most inverted at -2.5vols. JPY risk-reversals are also a pocket of acute stress, having steepened to multi-year highs.

Selling rich JPY skews looks compelling as the market is digesting Brexit and an uneventful Upper House election, and the attention turns to prospects of concerted balance sheet expansion and fiscal spending.

Even if the size of the fiscal package disappoints and USD/JPY resumes its grind lower on cleaner positioning, valuations, and historical back tests are supportive of short positions in JPY skews. We have previously noted the abrupt widening in JPY risk-reversals, especially leading into the Brexit, and found them to be at stretched levels.

JPY RRs have narrowed as JPY softened on chatters of “helicopter money”. Please be noted that this move, along with the pickup in USD/JPY since early July owes primarily to unwind of JPY longs and widening in USD vs JPY real rates spreads

The pairs which combine cheapest valuations and best historical returns are highlighted. We hold EUR/JPY 3M RR entered 20-Jun and picked up 1Y CAD/JPY and NZD/JPY RRs on 13-Jul. Sellers of JPY RRs will find their best prospects in EUR/JPY and CAD/JPY at the moment.