Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated

Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated  South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions

South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions  RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions

RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Goldman Sachs Delays Fed Rate Cut Forecast to 2026 Amid Rising Inflation Concerns

Goldman Sachs Delays Fed Rate Cut Forecast to 2026 Amid Rising Inflation Concerns  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty

Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects

DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects

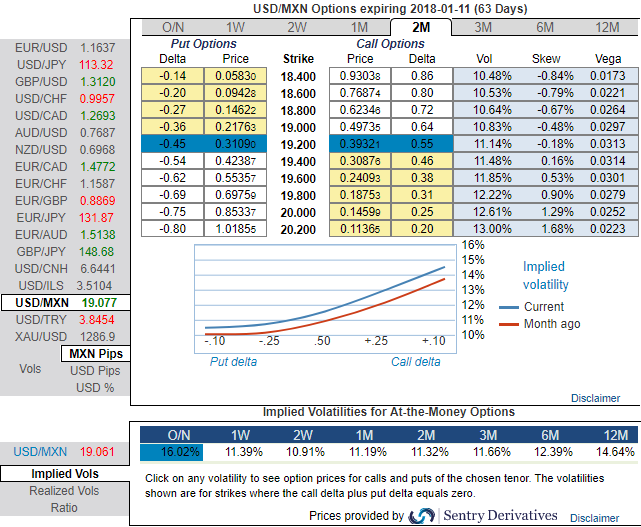

The Mexican central bank will likely leave its key rate unchanged at 7% once again, the meeting is unlikely to provide any surprises and should, therefore, be a non-event for the peso.

Please be noted that the current IVs of USDMXN is blowing out of the proportion, over 16% IVs are likely to collapse 11.5% in next 2w, 1m, and 2m tenors, and this has been a good news for the option writers.

However, positively skewed IVs of 2m tenors still indicates bullish risks, the telling statistic from the graphic is that that the static carry of delta hedged vega-neutral 2M skews is a very substantial 2.5 vol pt., near the upper-end of its 2-yr range.

However, if you have to observe the short-term technical trend of this pair, bearish sentiments have been mounting and slumps are most likely to test next strong supports at 18.90 levels.

Thus, the foreign traders and the investors may become a little more nervous and take a cautious approach towards MXN engagements.

The peso has come a long way from its Trump lows and screens overbought and overvalued at current levels, leading our LatAm team to turn underweight recently.

While the pair may head towards any directions with more potential on the downside in near term. According to this price behavior, we advocate options strategy as shown below that is likely optimized hedging motive.

Strategy: 3-Way Options straddle versus OTM call

Spread ratio: (Long 1: Long 1: Short 1)

How to execute: At spot reference: 1.6682, initiate long in GBPCAD 2M at the money +0.51 delta call, go long 2M at the money -0.49 delta put and simultaneously, short 2w (1%) out of the money call with positive theta. The short leg with narrowed expiry likely to reduce total hedging cost.

The standout feature of the USDMXN vol surface to us is the cheapness of risk-reversals, both vis-à-vis ATM vols and particularly relative to the amount of carry in forwards that allows for carry efficient expressions of bearish directional views or tail risk hedges.

Risks: Overall EM risk sentiment, higher UST rates or stubborn inflation could lead to the heavy long position being unwound along with debt portfolio outflows. An unfavorable NAFTA outcome is certain to structurally impair the currency.