RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions

RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions  BOJ Rate Hike Expectations Grow as Board Member Signals Hawkish Stance

BOJ Rate Hike Expectations Grow as Board Member Signals Hawkish Stance  Bank of England Set to Hold Interest Rates as Inflation Risks and Iran War Impact Loom

Bank of England Set to Hold Interest Rates as Inflation Risks and Iran War Impact Loom  AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says

AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says

Dovish Fed has led vols collapse, more in store: The collapse in vols following this week’s FOMC, even in longer tenors less influenced by event-related day-weights, says all one needs to know about the option market’s view of Fed policy.

The Goldilocks-like risk environment it seems to have ushered in may well keep the broad dollar in a range over coming months, trapped between a soft cap enforced by Fed gradualism that incentivizes investor flight away from quality, and a soft floor from the USD TWI’s already material under-pricing vis-à-vis interest rate differentials and the ever-present prospect of US fiscal/trade shocks. Coupled with the anti-populist outcome of the Dutch elections, we suspect this will unshackle investors who have hitherto been hesitant to enthusiastically embrace the reflation rally, and put even greater pressure on vols over the next 2-3 weeks.

Gamma vols are already extremely depressed after edging lower since the turn of the year, hence incremental vol selling interest should migrate out to longer expiries along curves that look extremely steep in a historical context (refer above chart).

We think the most vulnerable back-end vols are 1Y –18M expiries in EM currencies where curves are steep (refer above chart) and are either already fundamentally embraced by investors (BRL, RUB) or where a mix of lingering underweight positions and high beta to global equities holds out promise of sizeable inflows (KRW, ZAR).

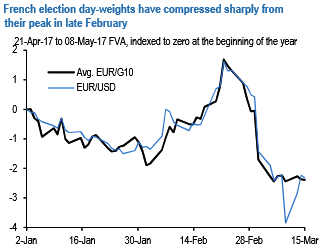

In addition to a more sanguine Fed outlook, a second factor that has weighed on vols recently is that day-weights for French elections have compressed sharply over the three weeks. EUR/G10 forward vols spanning both rounds of the election have fallen 3.8 % pts. on average(refer above chart), with the biggest declines concentrated in the most event sensitive pairs such as EURCHF and EURJPY (refer above chart).

Regarding politics, recent developments suggest that the U.S. administration continues to see their trade deficit as a problem and to seek redress the trade imbalance through bilateral negotiations. There are many political events in 2H of March and next month. The market focus will likely shift to politics after the FOMC and concerns on the U.S. protectionism will weigh on USD again in H2, as seen in early this year.

The Fed, in resisting the temptation to raise its estimate of where rates are heading in the long term, has reinforced its reputation as a dovish rate-setter. At least it is hiking, in sharp contrast to others. With the market reluctant to price in the pace of rate hikes the Fed is expecting to make, there's still a bit of life in the dollar rally – but not much and not for long. Meanwhile, there’s little here to really spook risk sentiment and risk-correlated currencies.