BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

The Swiss National Bank (SNB) has exhausted with an average of CHF 1.2bn. per week on FX market interventions in 2016, sources say. As a result, the Swiss central bank contributed decisively to keeping the EURCHF exchange rate above the 1.08 mark until October 2016.

Without its conformity, the exchange rate seems unlikely to have dropped to levels around 1.07. The appreciation pressure resting on the franc is undiminished as the continuous need for interventions illustrates.

However, it is unwise to admit the SNB going liberal with a remarkably stronger CHF near-term. The economic and inflationary trends remain too unstable for the SNB to be able to sit back and relax.

Even now the franc is putting pressure on the exporters’ margins and according to a newspaper poll amongst companies, the job cuts become more likely from their point of view – the strong rise of the PMI (the December index will be published today) could soon ease. And provide the SNB with an additional reason to continue to prevent CHF strengthening.

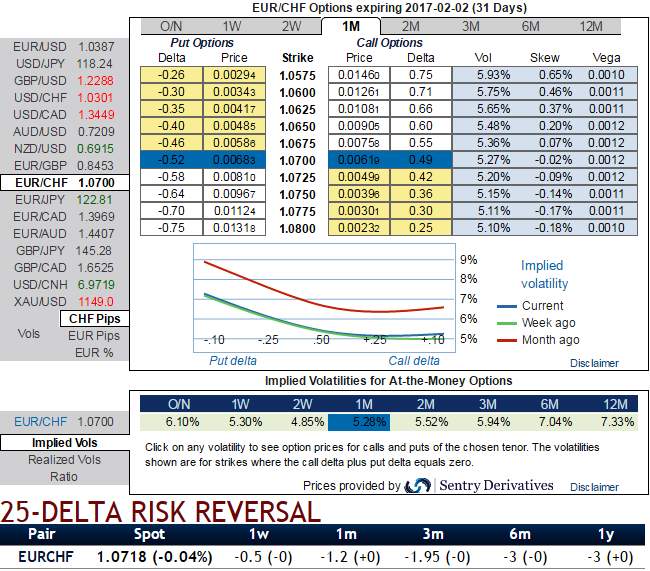

OTC Outlook and Hedging Framework:

Long lasted range bounded trend between upper strikes 1.1122 and lower strikes at around 1.0684 levels now comes to an end: EURCHF’s range bound pattern now seems like breaking out to make southward targets as bearish patterns with selling momentum are indicating weakness on both short and medium terms.

Please be informed that the implied volatilities of EURCHF ATM contracts of all expiries have still been the least among G10 currency segment. While positively skewed 1m IVs suggest the OTM put are on higher demand.

While, the 25-delta risk of reversal of EURCHF has also been indicating bearish pressures both in short and long run, seems to be one of the pairs to be hedged for downside risks as it indicates puts have been relatively costlier.

FX Option Trading Strategy:

Strategy: 3-Way Diagonal Straddle versus OTM Call

Spread ratio: (Long 1: Long 1: Short 1)

The execution: Initiate long in EURCHF 1M at the money -0.49 delta put, long in 1M at the money +0.51 delta call and simultaneously, Short theta in 2w (1.5%) out of the money call with positive theta or closer to zero. Theta is positive; time decay is bad for a buyer, but good for an option writer.

Rationale: Let’s glance on sensitivity tool for put options of this pair, it flashes up higher probabilistic numbers for OTM put strikes which would mean that higher likelihood of expiring these contracts in-the-money, hence, it wise to deploy positions against this signals (i.e writing an OTM call with shorter tenors).