Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025

Since the Brexit referendum and the 2016 US election, the two major upsets during the turbulent 2016, FX option markets have been sensitive on the issue of political event risk premium. The upcoming 2020 US election pricing are gearing to be one of the most eventful in history and as one possible driver capable of breaking the fragile state that global economy lies in at the moment.

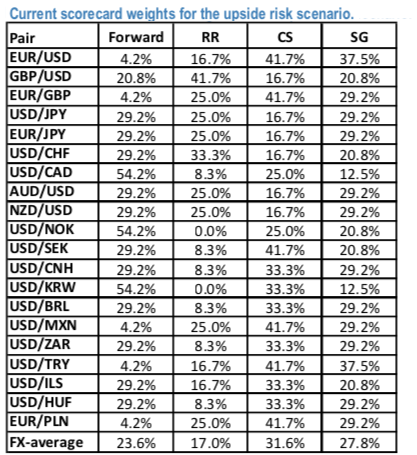

We referred to the JP Morgan’s newly introduced scorecard for selecting the best FX hedging instruments, for different currencies and over time. Skipping all technical details, the idea behind the model was just to highlight how different instruments could perform based on the relative interplay of different pricing parameters, allowing an optimal allocation as a function of time. The note has attracted the interest of several real money players, especially in the EUR-area, looking for viable solutions at a time when elevated (although slightly declining vs. Q4 2018) fwd points and flat yield curves implied heavy costs if implementing hedges via forwards.

We refer to the earlier piece for a more comprehensive review of the approach. The recent flip in the sign of the riskies cut the weight associated with riskies based on the rules of the scorecard. For GBPUSD risk-reversals get the highest allocation (41.7%) given the negative skew.

At present, the scorecard approach (refer above nutshell) favours call spreads (16.7% on average) and seagulls (20.8%) over forwards (20.8%) and risk-reversals (41.7%).

On GBPUSD upside, the JP Morgan’s scorecard approach has also largely outperformed the benchmark forward since 2014.

Forward points remain a factor impacting long forward positions, although less harmful than for EURUSD given the tighter carry.

Momentum has recently waned on GBP, with price remaining in a tight range over the past few weeks.

Sign of the skew well in negative territory favours “bullish” (i.e. long GBP calls and short GBP puts) risk- reversals over spread structures for playing GBP strength over medium horizons:

Sell 6m 25-delta risk-reversal (sell GBP put, buy GBP call) on GBPUSD at 1.3/1.6 vols indicative. Courtesy: JPM