FxWirePro: USD/CNY slips as strong China exports data Lift yuan

FxWirePro: USD/CNY slips as strong China exports data Lift yuan  FxWirePro: GBP/USD eases as dollar firms ahead of U.S. June non-farm payrolls report

FxWirePro: GBP/USD eases as dollar firms ahead of U.S. June non-farm payrolls report  NZDJPY Bullish Above 93 as Yen Stumbles – Buy Signal Triggers at 93.50

NZDJPY Bullish Above 93 as Yen Stumbles – Buy Signal Triggers at 93.50  FxWirePro: USD/JPY advances as traders test Japan's intervention resolve

FxWirePro: USD/JPY advances as traders test Japan's intervention resolve  FxWirePro : EUR/NZD slips lower after soft US jobs report

FxWirePro : EUR/NZD slips lower after soft US jobs report  Bitcoin Reclaims $65,000 as Easing Geopolitical Tensions Fuel Risk-On Rally

Bitcoin Reclaims $65,000 as Easing Geopolitical Tensions Fuel Risk-On Rally  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data

FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data  NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop

NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop  FxWirePro: EUR/AUD slips after surprise U.S. employment data

FxWirePro: EUR/AUD slips after surprise U.S. employment data  FxWirePro: EUR/ AUD neutral in the near term, scope further downside

FxWirePro: EUR/ AUD neutral in the near term, scope further downside  FxWirePro : USD/CAD falls as strong Canadian jobs data lifts loonie

FxWirePro : USD/CAD falls as strong Canadian jobs data lifts loonie  AUDJPY Bears Poised: Sell Rallies at 111.55 for 108 Target with 112.20 Stop

AUDJPY Bears Poised: Sell Rallies at 111.55 for 108 Target with 112.20 Stop  FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data

FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data  AUDJPY Rebounds on Yen Weakness – Bullish Buy Setup Above 112 Targets 115

AUDJPY Rebounds on Yen Weakness – Bullish Buy Setup Above 112 Targets 115  FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar

FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar

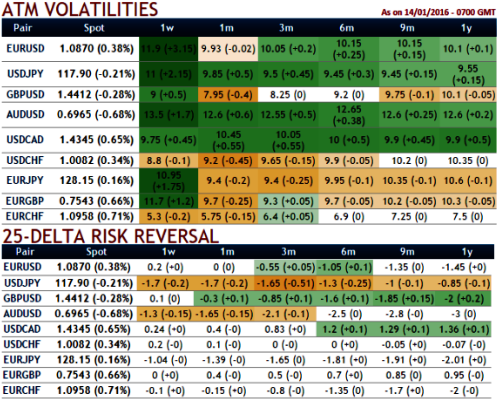

As you can observe from the table showing implied volatilities of ATM contracts edging higher which is highest among G10 currency space (EURUSD of 1W-1M expiries show 11.9% and 9.93%).

While risk reversal is seen positive numbers for next 1 week to 1 month's expiries, which means that an aggressively out of the money (OTM) option is often seen as a speculative bet/hedge that the currency will move sharply in the direction of the strike price.

It is unlikely for higher EURO's sustainability until there is real domestically generated inflation.

Any spikes in this pair in near term can be attributed as shorting opportunity in our back spreads.

So, by employing the Vega options can not only multiply the returns but also upbeat the implied volatility.

As shown in the diagram, contemplating the above risk reversal computations, we construct strategy comprising of both ITM as well as ATM puts in the ratio of 2:1 so as to suit the swings on either directions.

Capitalizing on higher IV and reasonnnable risk reversals in short run, ITM puts are attractive for shorting, so we can eye on shorting 1W (1%) in the money put that would lock in certain yields by initial receipts of premiums as upswings are likely in this pair.

Thereafter, go long in 2 lots of 1m ATM -0.48 delta puts with vega 124.62 are preferred to suit the long term losing streaks, thereby the spread would be executed for net debit and the cost is reduced by short side.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: EUR/USD diagonal PRBS for hedging swings with reduced

Thursday, January 14, 2016 1:49 PM UTC

Editor's Picks

- Market Data

Most Popular