Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?

BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?  Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings

Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

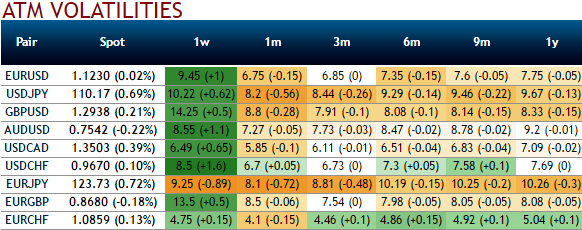

After ECB’s monetary policy session, euro vols have collapsed, let’s have a glance through the implied volatilities of EURCHF ATM contracts from the above nutshell, IVs of this underlying pair of all expiries have still been the least among G10 currency segment. These lower volatile conditions are conducive for the option writers.

The options with a higher IV cost more which is why in this case OTM puts have been preferred over ATM instruments. This is intuitive due to the higher likelihood of the market ‘swinging’ in your favor. If IV increases and you are holding an option, this is good.

Please also be noted that the 25-delta risk of reversal of EURCHF has also not been indicating any dramatic shoot up nor any slumps, but seems to be one of the pairs to be hedged for downside risks in the long run as it indicates puts have been relatively costlier.

On a broader perspective, technically please be noted that the every attempt of upswings have constantly been hindered below 21EMAs, bears sensing major resistances at this level with MACD remaining in bearish trajectory, while RSI and stochastic signal fading strength in rallies on monthly terms.

Consequently, it is also spotted out that the downward convergence thereafter between price curve and leading oscillators. Almost same is the case on weekly plotting (fading strength on RSI at 63 levels).

Overall, the non-directional trend likely to persist in major trend but with little weakness is on cards.

But on the contrary, gradual euro strength should nudge EURCHF higher but significantly. As a result, chances of calls being priced exorbitantly could be expected on account of the second round of European political risks (Italian elections).

For now, we could still foresee range bounded trend to persist in near future but little weakness in near-term is puzzling bulls of this pair to drag southward targets but very much within above-stated range.

As a result, we recommend below option strategies using right options, thereby, one can benefit from certain returns.

Naked Strangle Shorting:

Short 2m OTM put (2% strike difference referring lower cap) and short OTM call simultaneously of the same expiry (2% strike referring upper cap) (we reiterate, comparatively short term for maturity is desired).

Overview: Slightly bearish in short term but sideways in medium term.

Timeframe: 3 months

When you write an option, the seller wants IV to remain lower level or to shrink so the premium also fades away.

Hence, writing such calls seems smart choice in tepid IVs on speculative or trading grounds.

Considering above OTC market reasoning, amid prevailing uptrend we think downside risks can also not to be disregarded in the long term, as result we reckon deploying shorts in such exorbitant call options.