South Korea Central Bank Signals Inflation Concerns as Oil Prices Surge

South Korea Central Bank Signals Inflation Concerns as Oil Prices Surge  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty

Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty  ECB Rate Outlook: Ceasefire Eases Pressure but Hikes Still Expected in 2026

ECB Rate Outlook: Ceasefire Eases Pressure but Hikes Still Expected in 2026  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve

ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve  BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns

BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

The fate of the greenback depends on much more on a far more important issue at present: Janet Yellen’s successor as Fed Chair. The FOMC’s monetary policy decisions are not taken at the Chair’s discretion. But let’s not fool ourselves. Over the past decades, the Chairs considerably influenced US monetary policy. Paul Volcker, who ended high inflation but in return caused the double recession of 1980/82.

A higher USDJPY relies on US TIPS yields breaking free; we think a test of December’s peak is possible but a break higher is unlikely. It’s also increasingly apparent that yen bears can’t rely on a risk-friendly backdrop alone to help them, given unhelpful cross-currency basis spreads. We’re happy with long USDJPY during the current rising trend in TIPS yields but we’ve lost almost all hope of seeing 120 again and there’s a long-term danger of a move lower, towards PPP-consistent levels closer to 100.

The Bank of Canada has started to normalize monetary policy as an offset to a hot property market, and the CAD has recovered in recent months. But it’s still cheap relative to AUD and NZD and relative to the USD.

Both EUR and JPY are undervalued against the US dollar because getting (and keeping) the currency down has been a policy priority of both ECB and BOJ. Europe’s economy is recovering a little faster than Japan’s and inflation expectations have moved further away from zero, which has allowed the ECB to shift its focus towards slowing bond purchases and normalizing policy far sooner than the BOJ will. We’ve seen EURJPY rally sharply but the current correction offers a chance of a second bite at the cherry. We’re looking for a test of the post-1980- resistance line at 141.

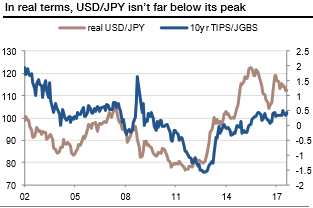

The above chart shows the spread between TPS and JGBs, against an inflation-adjusted USDJPY. Abenomics and BOJ policy took the yen from very overvalued levels to undervalued ones, and has kept it there. It’s not obvious if keeping there would have been possible without a recovery in US Treasury yields in both real and nominal terms, outright and relative to JGBs. As with the ECB, the BOJ will in due course shift focus towards policy normalization but for now, inflation expectations are still much lower (0.3%) than in the US (2.3%) or the Euro area (1.6%).

As a propensity for consolidating within the triangle pattern, USDJPY has most likely peaked in 2015 at the multi-decade trend line resistance (then at 126, now at 123).

The 10y TIPS yield is grinding higher after encountering support near the 5-year trend line support at 0.25%/0.20%.

Our measure of USDCAD PPP is around 1.15, suggesting there’s some more room for CAD to out-perform the US Dollar. More importantly though, now that Alberta’s economy has stabilized, the bank of Canada is focusing on policy normalization and taming a (too) strong property market. Canada escaped the worst of the global financial crisis has no domestic (non-FX) need for emergency levels of rates. Getting CADJPY back to the previous peak levels in real terms would see spot around 100.

A 10% move higher in EURJPY would take it back to 2007 and 2014 levels in real terms. Yield differentials are steadily moving in the euro’s favor and that trend will continue as long as the BOJ keeps JGB yields depressed. EURJPY ‘fair value’ is around 137, so there’s a bit further to go on that basis, but that big differentiator is that the ECB is minded to begin policy normalization much earlier than the BOJ. Courtesy: JPM