Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?

BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate

Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation

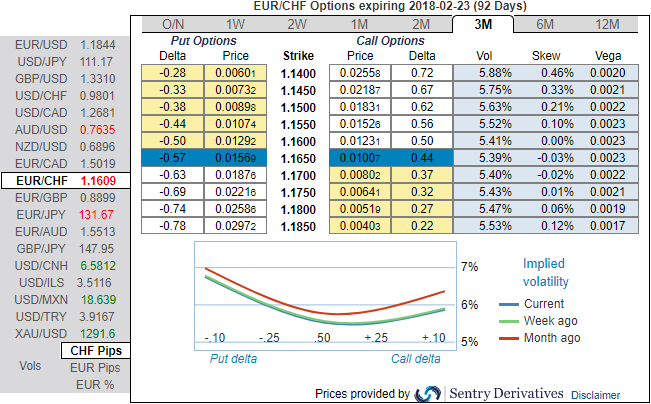

Long EURCHF has been encouraged on account of the underperformance of Swiss franc this week is a response the upward pressure on global bond yields; it is not a beta move to EURUSD as such.

We continue to doubt quite how much domestic capital is leaking from CHF, certainly in the direction of EUR, and so remain rather circumspect about the ultimate targets for EURCHF.

But at the same time, we recognize the speculative interest to sell CHF as a monetary laggard (we won’t mention here that the SNB has completed its QE even before the ECB has announced its plans to taper) and suspect short-term spec selling can sustain another 1-2% rally in EURCHF.

Before we proceed through the core part of the options strategy, let’s glance through the implied volatilities of EURCHF ATM contracts from the above nutshell, IVs of this underlying pair of all expiries have still been the least among G10 currency segment despite the ECB’s monetary policy announcement and other upcoming data events. These lower volatile conditions are conducive for the option writers.

Despite uptrend that we’ve been seeing in EURCHF, positively skewed IVs indicate hedgers’ interests well balanced for both OTM calls and put bids. Please also be noted that the 25-delta risk of reversal of EURCHF has also not been indicating any dramatic shoot up nor any slumps, but bearish neutral risk reversals indicate that this pair to have been hedged for the downside risks as it indicates puts have been relatively costlier.

Thus, in order to sync with the above fundamental factors, the technical trend of the underlying price and the OTC indications, we advocate the below options strategy.

From the above technical chart, it is clearly understood that the upside risks are on cards. As a result, ITM calls have been in high demand.

We formulate suitable hedging framework contemplating all the above aspects. Place call ratio spread with 1:2 ratios.

How to execute: At spot reference: 1.1610, buy ITM (1.1480) +0.66 delta call with longer expiry (let’s say, 2m tenor). Sell two lots of OTM strike calls (1.2065) of comparatively narrowed tenors (say 1m). Thereby, we’ve formulated the strategy so as to sync ongoing technical trend with the delta risk reversal.

The delta value becomes more and more insensitive as the EURCHF falls lower and lower and hence on the lower side, the delta value is zero.

On the higher side, it increases in the magnitude but remains negative indicating the negative effect on the options trader position with the pair rallying.

Why call ratio spread: As the pair has made steep slumps and healthy recovery we see a neutral to bearish environment when you are projecting decreasing volatility (see from next 1 month to 3 months it’s been gradually reducing)

Risk/Reward Profile: The risk is unlimited. The reward is the difference in the strike prices plus the net credit, multiplied by the number of long contracts.